Best Crypto Savings Account 2026: Top Platforms Compared

Best Crypto Savings Account 2026: Top Platforms Compared

Best Crypto Savings Account 2026: Top Platforms Compared

Best Crypto Savings Account 2026: Top Platforms Compared

Finding the best crypto savings account in 2026 matters more than ever. Traditional savings rates still struggle to keep pace with inflation, while crypto savings accounts offer compelling alternatives for investors willing to navigate digital assets. This guide examines the top options available, compares them to traditional high-yield savings accounts, and helps you decide where to park your funds.

The crypto savings space has matured a lot since the turbulent events of 2022 and 2023. The industry now has stronger safeguards, clearer regulations, and more transparent operations. For investors seeking higher yields without active trading, a crypto savings account offers a middle ground between traditional finance and the volatile world of crypto speculation.

Key takeaways

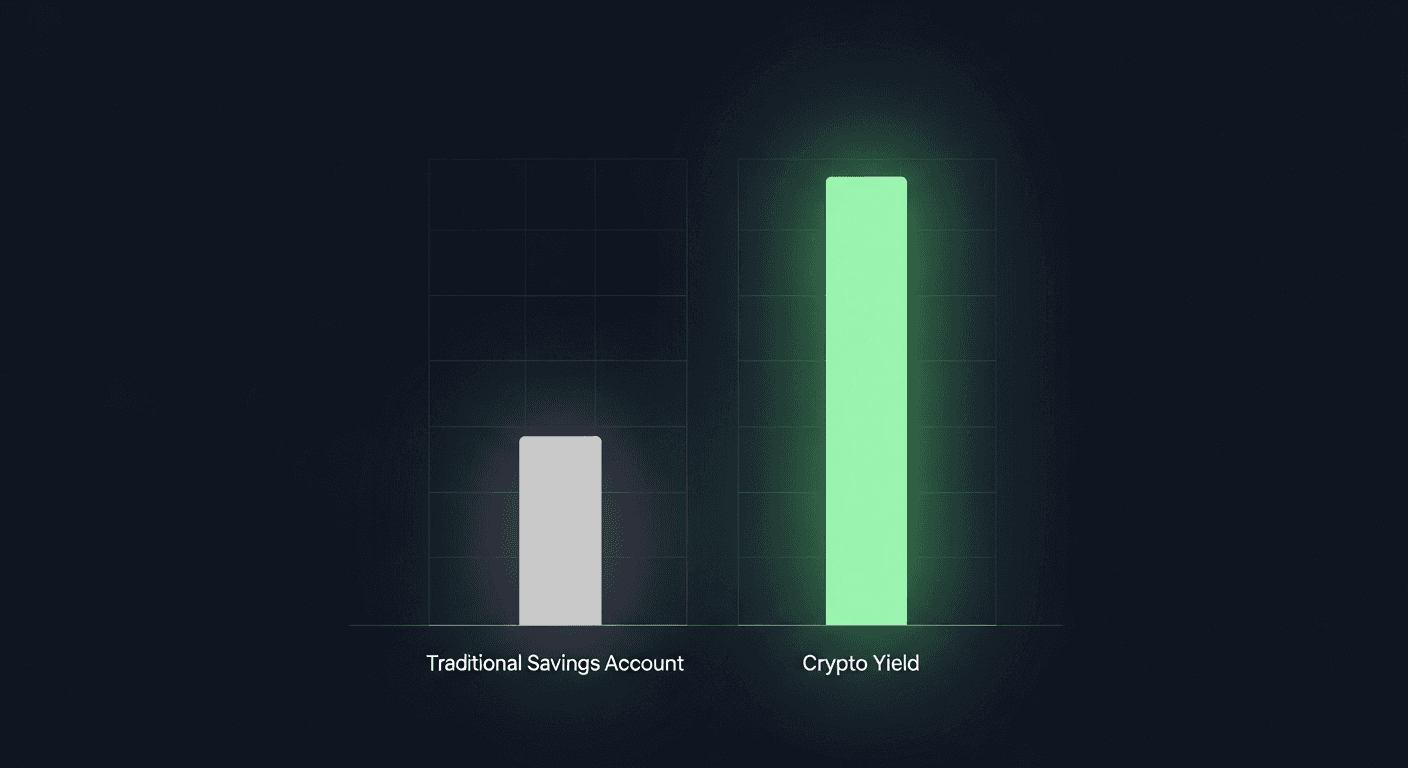

Crypto savings accounts offer yields ranging from 4% to 12% APY, higher than traditional savings accounts averaging 4-5% APY in 2026

Risk management has improved: institutional-grade custody, proof of reserves, and regulatory compliance are now industry standards

Stablecoins provide a lower-volatility entry point for those wanting crypto yields without Bitcoin price exposure

Tax reporting integration has become essential as regulatory scrutiny increases globally

Platform selection matters: security, transparency, and fee structures vary dramatically between providers

Crypto savings vs traditional high-yield savings accounts: 2026 comparison

Before diving into specific platforms, it's worth understanding how crypto savings accounts stack up against the best savings account options in traditional finance.

Traditional high-yield savings accounts

The high yield savings account market in 2026 offers rates between 4% and 5.25% APY at leading online banks. These accounts benefit from FDIC insurance up to $250,000, making them essentially risk-free for qualifying deposits. Rates remain subject to Federal Reserve policy and typically lag behind inflation during expansionary periods.

Advantages:

FDIC insurance protection

Zero principal risk

Easy access through traditional banking infrastructure

No learning curve required

Limitations:

Yields capped by central bank policy

Returns may not outpace inflation

Limited flexibility in account structures

No exposure to potential asset appreciation

Crypto savings accounts

A crypto savings account operates differently. You deposit cryptocurrency (or purchase it through the platform), and the platform generates yield through various mechanisms: lending to institutions, participating in decentralized finance protocols, or staking proof-of-stake cryptocurrencies.

Advantages:

Higher potential yields (often 2-3x traditional rates)

Multiple asset options (Bitcoin, Ethereum, stablecoins)

Potential for principal appreciation (on non-stablecoin deposits)

Access to emerging financial infrastructure

Limitations:

No government insurance on deposits

Smart contract and platform risk

Regulatory uncertainty in some jurisdictions

Requires understanding of crypto fundamentals

The crypto vs savings account decision

When evaluating crypto vs savings accounts, the decision comes down to your risk tolerance, investment timeline, and financial goals. Many sophisticated investors now use both: keeping emergency funds in traditional FDIC-insured accounts while allocating a portion of longer-term savings to crypto interest accounts for better yields.

Top crypto savings options in 2026: platform comparison

The following comparison table outlines leading platforms offering bitcoin savings account and broader crypto savings functionality:

Platform | Stablecoin APY | BTC APY | ETH APY | Insurance/Protection | Minimum Deposit | Key Differentiator |

|---|---|---|---|---|---|---|

Pistachio.fi | 6-10% | 4-7% | 5-9% | Institutional custody | None | Curated vaults, gasless transactions |

Nexo | 5-8% | 3-5% | 4-6% | Proof of reserves | $100 | Wide asset selection |

Ledn | 4-7% | 2-4% | 3-5% | Partial insurance | $500 | Regulatory licenses |

DeFi Protocols | 7-12% | 5-8% | 6-10% | Smart contract audits | None | DeFi-native yields |

Coinbase | 5-6% | 3-4% | 4-5% | FDIC on USD | $1 | Exchange integration |

Note: APY rates fluctuate based on market conditions. Figures represent typical ranges as of early 2026.

Understanding the yield differences

The variation in yields across platforms reflects different risk profiles and yield-generation strategies. Platforms offering higher returns typically deploy assets into DeFi protocols, which carry smart contract risk but access deeper liquidity pools. More conservative platforms may lend primarily to institutional borrowers or use simpler staking mechanisms.

This is why high yield crypto savings requires careful platform evaluation. A platform advertising 15%+ yields on stablecoins should prompt questions about sustainability and risk exposure. The industry learned these lessons painfully in previous market cycles.

What to look for when choosing a crypto savings platform

Selecting the right crypto savings account requires evaluating several factors. The platform you choose becomes the custodian of your assets, so due diligence matters.

1. Security infrastructure

Security should be your primary consideration. Look for platforms offering:

Institutional-grade custody: Assets held with established custodians like Fireblocks, BitGo, or Coinbase Custody

Multi-signature wallets: Requiring multiple approvals for asset movement

Cold storage: Majority of assets kept offline

Regular security audits: Third-party verification of security practices

Bug bounty programs: Incentivizing white-hat hackers to identify vulnerabilities

Pistachio.fi implements institutional custody solutions, so your assets receive the same protection that institutional investors demand.

2. Risk transparency

The best platforms provide clear information about how they generate yield and what risks are involved. Key indicators include:

Published risk grades: Every investment option should have an associated risk rating

Strategy documentation: Clear explanation of yield sources

Proof of reserves: Regular attestations of asset holdings

Audit reports: Both financial and smart contract audits

Risk grades help investors match opportunities to their risk tolerance. Without this transparency, you're investing blind.

3. Fee structure

Hidden fees can eat into your returns. Evaluate:

Deposit/withdrawal fees: Some platforms charge network fees or flat fees

Management fees: Annual percentages taken from yields

Gas costs: On platforms requiring blockchain transactions

Spread on conversions: If exchanging between assets

Gasless platforms like Pistachio.fi eliminate transaction fees entirely, so more of your yield reaches your wallet instead of disappearing into network costs.

4. Tax reporting capabilities

As crypto taxation becomes more stringent globally, seamless tax reporting has shifted from convenience to necessity. Look for:

Transaction history exports: Complete records in standard formats

Tax software integration: Direct connections to crypto tax platforms

Gain/loss calculations: Automated cost basis tracking

Jurisdiction-specific reports: Formatted for your country's requirements

Awaken.Tax integration, as offered by Pistachio.fi, provides one-click tax export. That saves hours of manual reconciliation and reduces costly reporting errors.

5. Platform usability and support

Even the most secure platform fails if you can't effectively use it:

Intuitive interface: Clear navigation and transaction flows

Mobile access: Responsive design or dedicated apps

Customer support: Responsive help when issues arise

Educational resources: Helping you understand products and risks

Curated investment vaults simplify the experience by offering expert-selected protocols rather than overwhelming you with hundreds of options requiring individual evaluation.

Understanding and managing crypto savings risks

Let's be honest about the risks. While the industry has matured, significant risks remain that differentiate these products from traditional bank accounts.

Platform risk

The biggest risk is the platform itself. History has shown that even major crypto platforms can fail due to fraud, mismanagement, or unsustainable business models. To mitigate this:

Diversifying across multiple platforms

Choosing platforms with regulatory licenses

Verifying proof of reserves independently

Starting with smaller amounts before committing significant capital

Smart contract risk

Platforms generating yield through DeFi protocols expose users to smart contract vulnerabilities. Even audited contracts can contain exploitable bugs. To protect yourself:

Favoring platforms using battle-tested protocols

Checking audit histories and bug bounty programs

Understanding that higher yields often correlate with newer, less-tested contracts

Market risk

For non-stablecoin deposits, you face cryptocurrency price volatility. A 10% APY means nothing if the underlying asset loses 50% of its value. Consider:

Using stablecoins for pure yield strategies

Only depositing crypto you intend to hold long-term regardless

Understanding that crypto savings accounts don't eliminate market risk

Regulatory risk

The regulatory landscape continues evolving. Potential impacts include:

Platform restrictions in certain jurisdictions

Tax treatment changes affecting net returns

Licensing requirements limiting platform options

Liquidity risk

Some high-yield options require locking assets for specified periods. Ensure you understand:

Withdrawal timeframes and any associated penalties

Whether your funds are accessible during market stress

Lock-up periods for higher-yield tiers

Frequently asked questions

Are crypto savings accounts safe in 2026?

Crypto savings accounts have become safer than in previous years, but they're not equivalent to FDIC-insured bank accounts. The best platforms now offer institutional-grade custody, regular audits, and proof of reserves. Risks remain including platform failure, smart contract vulnerabilities, and market volatility. Safety depends largely on choosing reputable platforms with strong security infrastructure and transparent operations.

How are crypto savings account earnings taxed?

In most jurisdictions, interest earned from crypto savings accounts is taxable income, similar to traditional savings account interest. The complexity increases because you're often earning crypto rather than fiat currency, requiring valuation at the time of receipt. If you deposit volatile cryptocurrencies, you may face capital gains implications on the principal. Integrated tax reporting features have become essential for accurate compliance.

Can I lose money in a crypto savings account?

Yes, you can lose money in several ways: the platform could fail or be hacked, smart contracts could be exploited, or (for non-stablecoin deposits) the underlying cryptocurrency could decline in value. Unlike traditional bank accounts, no government insurance protects crypto savings deposits. This is why risk assessment, platform selection, and portfolio diversification remain critical.

What's the difference between staking and crypto savings accounts?

Staking involves locking specific proof-of-stake cryptocurrencies to help validate blockchain transactions, earning rewards in return. Crypto savings accounts are broader products that may use staking as one yield-generation method among many, including lending, liquidity provision, and DeFi protocol participation. Savings accounts typically offer more flexibility and may provide yield on assets that can't be directly staked.

How much should I put in a crypto savings account?

Financial advisors generally recommend limiting crypto exposure to an amount you can afford to lose, often suggested as 5-15% of investable assets for those comfortable with higher risk. Within that crypto allocation, savings accounts can be appropriate for funds you don't need for active trading. Never deposit emergency funds or money you'll need short-term into crypto savings accounts, regardless of the yield offered.

Start earning higher yields today

The crypto savings landscape has evolved, offering investors more secure, transparent, and user-friendly options than before. While risks remain, choosing the right platform dramatically improves your risk-adjusted returns.

Pistachio.fi addresses the traditional barriers that have kept many investors from accessing crypto yield:

Curated Investment Vaults remove the complexity of evaluating hundreds of protocols

Expert Risk Grades on every option help you match investments to your comfort level

Completely Gasless transactions mean zero fees eating into your returns

Awaken.Tax Integration provides one-click tax export for stress-free compliance

Elite Security with institutional-grade custody protects your assets

Whether you're exploring crypto savings for the first time or optimizing an existing strategy, the platform you choose makes all the difference.

Related reading

Ready to put your crypto to work?

Visit Pistachio.fi to explore curated yield opportunities with institutional-grade security and zero transaction fees. Your journey to smarter crypto savings starts with a single click.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Cryptocurrency investments carry significant risks including potential loss of principal. Past performance does not guarantee future results. Always conduct your own research and consider consulting a financial advisor before making investment decisions.

Finding the best crypto savings account in 2026 matters more than ever. Traditional savings rates still struggle to keep pace with inflation, while crypto savings accounts offer compelling alternatives for investors willing to navigate digital assets. This guide examines the top options available, compares them to traditional high-yield savings accounts, and helps you decide where to park your funds.

The crypto savings space has matured a lot since the turbulent events of 2022 and 2023. The industry now has stronger safeguards, clearer regulations, and more transparent operations. For investors seeking higher yields without active trading, a crypto savings account offers a middle ground between traditional finance and the volatile world of crypto speculation.

Key takeaways

Crypto savings accounts offer yields ranging from 4% to 12% APY, higher than traditional savings accounts averaging 4-5% APY in 2026

Risk management has improved: institutional-grade custody, proof of reserves, and regulatory compliance are now industry standards

Stablecoins provide a lower-volatility entry point for those wanting crypto yields without Bitcoin price exposure

Tax reporting integration has become essential as regulatory scrutiny increases globally

Platform selection matters: security, transparency, and fee structures vary dramatically between providers

Crypto savings vs traditional high-yield savings accounts: 2026 comparison

Before diving into specific platforms, it's worth understanding how crypto savings accounts stack up against the best savings account options in traditional finance.

Traditional high-yield savings accounts

The high yield savings account market in 2026 offers rates between 4% and 5.25% APY at leading online banks. These accounts benefit from FDIC insurance up to $250,000, making them essentially risk-free for qualifying deposits. Rates remain subject to Federal Reserve policy and typically lag behind inflation during expansionary periods.

Advantages:

FDIC insurance protection

Zero principal risk

Easy access through traditional banking infrastructure

No learning curve required

Limitations:

Yields capped by central bank policy

Returns may not outpace inflation

Limited flexibility in account structures

No exposure to potential asset appreciation

Crypto savings accounts

A crypto savings account operates differently. You deposit cryptocurrency (or purchase it through the platform), and the platform generates yield through various mechanisms: lending to institutions, participating in decentralized finance protocols, or staking proof-of-stake cryptocurrencies.

Advantages:

Higher potential yields (often 2-3x traditional rates)

Multiple asset options (Bitcoin, Ethereum, stablecoins)

Potential for principal appreciation (on non-stablecoin deposits)

Access to emerging financial infrastructure

Limitations:

No government insurance on deposits

Smart contract and platform risk

Regulatory uncertainty in some jurisdictions

Requires understanding of crypto fundamentals

The crypto vs savings account decision

When evaluating crypto vs savings accounts, the decision comes down to your risk tolerance, investment timeline, and financial goals. Many sophisticated investors now use both: keeping emergency funds in traditional FDIC-insured accounts while allocating a portion of longer-term savings to crypto interest accounts for better yields.

Top crypto savings options in 2026: platform comparison

The following comparison table outlines leading platforms offering bitcoin savings account and broader crypto savings functionality:

Platform | Stablecoin APY | BTC APY | ETH APY | Insurance/Protection | Minimum Deposit | Key Differentiator |

|---|---|---|---|---|---|---|

Pistachio.fi | 6-10% | 4-7% | 5-9% | Institutional custody | None | Curated vaults, gasless transactions |

Nexo | 5-8% | 3-5% | 4-6% | Proof of reserves | $100 | Wide asset selection |

Ledn | 4-7% | 2-4% | 3-5% | Partial insurance | $500 | Regulatory licenses |

DeFi Protocols | 7-12% | 5-8% | 6-10% | Smart contract audits | None | DeFi-native yields |

Coinbase | 5-6% | 3-4% | 4-5% | FDIC on USD | $1 | Exchange integration |

Note: APY rates fluctuate based on market conditions. Figures represent typical ranges as of early 2026.

Understanding the yield differences

The variation in yields across platforms reflects different risk profiles and yield-generation strategies. Platforms offering higher returns typically deploy assets into DeFi protocols, which carry smart contract risk but access deeper liquidity pools. More conservative platforms may lend primarily to institutional borrowers or use simpler staking mechanisms.

This is why high yield crypto savings requires careful platform evaluation. A platform advertising 15%+ yields on stablecoins should prompt questions about sustainability and risk exposure. The industry learned these lessons painfully in previous market cycles.

What to look for when choosing a crypto savings platform

Selecting the right crypto savings account requires evaluating several factors. The platform you choose becomes the custodian of your assets, so due diligence matters.

1. Security infrastructure

Security should be your primary consideration. Look for platforms offering:

Institutional-grade custody: Assets held with established custodians like Fireblocks, BitGo, or Coinbase Custody

Multi-signature wallets: Requiring multiple approvals for asset movement

Cold storage: Majority of assets kept offline

Regular security audits: Third-party verification of security practices

Bug bounty programs: Incentivizing white-hat hackers to identify vulnerabilities

Pistachio.fi implements institutional custody solutions, so your assets receive the same protection that institutional investors demand.

2. Risk transparency

The best platforms provide clear information about how they generate yield and what risks are involved. Key indicators include:

Published risk grades: Every investment option should have an associated risk rating

Strategy documentation: Clear explanation of yield sources

Proof of reserves: Regular attestations of asset holdings

Audit reports: Both financial and smart contract audits

Risk grades help investors match opportunities to their risk tolerance. Without this transparency, you're investing blind.

3. Fee structure

Hidden fees can eat into your returns. Evaluate:

Deposit/withdrawal fees: Some platforms charge network fees or flat fees

Management fees: Annual percentages taken from yields

Gas costs: On platforms requiring blockchain transactions

Spread on conversions: If exchanging between assets

Gasless platforms like Pistachio.fi eliminate transaction fees entirely, so more of your yield reaches your wallet instead of disappearing into network costs.

4. Tax reporting capabilities

As crypto taxation becomes more stringent globally, seamless tax reporting has shifted from convenience to necessity. Look for:

Transaction history exports: Complete records in standard formats

Tax software integration: Direct connections to crypto tax platforms

Gain/loss calculations: Automated cost basis tracking

Jurisdiction-specific reports: Formatted for your country's requirements

Awaken.Tax integration, as offered by Pistachio.fi, provides one-click tax export. That saves hours of manual reconciliation and reduces costly reporting errors.

5. Platform usability and support

Even the most secure platform fails if you can't effectively use it:

Intuitive interface: Clear navigation and transaction flows

Mobile access: Responsive design or dedicated apps

Customer support: Responsive help when issues arise

Educational resources: Helping you understand products and risks

Curated investment vaults simplify the experience by offering expert-selected protocols rather than overwhelming you with hundreds of options requiring individual evaluation.

Understanding and managing crypto savings risks

Let's be honest about the risks. While the industry has matured, significant risks remain that differentiate these products from traditional bank accounts.

Platform risk

The biggest risk is the platform itself. History has shown that even major crypto platforms can fail due to fraud, mismanagement, or unsustainable business models. To mitigate this:

Diversifying across multiple platforms

Choosing platforms with regulatory licenses

Verifying proof of reserves independently

Starting with smaller amounts before committing significant capital

Smart contract risk

Platforms generating yield through DeFi protocols expose users to smart contract vulnerabilities. Even audited contracts can contain exploitable bugs. To protect yourself:

Favoring platforms using battle-tested protocols

Checking audit histories and bug bounty programs

Understanding that higher yields often correlate with newer, less-tested contracts

Market risk

For non-stablecoin deposits, you face cryptocurrency price volatility. A 10% APY means nothing if the underlying asset loses 50% of its value. Consider:

Using stablecoins for pure yield strategies

Only depositing crypto you intend to hold long-term regardless

Understanding that crypto savings accounts don't eliminate market risk

Regulatory risk

The regulatory landscape continues evolving. Potential impacts include:

Platform restrictions in certain jurisdictions

Tax treatment changes affecting net returns

Licensing requirements limiting platform options

Liquidity risk

Some high-yield options require locking assets for specified periods. Ensure you understand:

Withdrawal timeframes and any associated penalties

Whether your funds are accessible during market stress

Lock-up periods for higher-yield tiers

Frequently asked questions

Are crypto savings accounts safe in 2026?

Crypto savings accounts have become safer than in previous years, but they're not equivalent to FDIC-insured bank accounts. The best platforms now offer institutional-grade custody, regular audits, and proof of reserves. Risks remain including platform failure, smart contract vulnerabilities, and market volatility. Safety depends largely on choosing reputable platforms with strong security infrastructure and transparent operations.

How are crypto savings account earnings taxed?

In most jurisdictions, interest earned from crypto savings accounts is taxable income, similar to traditional savings account interest. The complexity increases because you're often earning crypto rather than fiat currency, requiring valuation at the time of receipt. If you deposit volatile cryptocurrencies, you may face capital gains implications on the principal. Integrated tax reporting features have become essential for accurate compliance.

Can I lose money in a crypto savings account?

Yes, you can lose money in several ways: the platform could fail or be hacked, smart contracts could be exploited, or (for non-stablecoin deposits) the underlying cryptocurrency could decline in value. Unlike traditional bank accounts, no government insurance protects crypto savings deposits. This is why risk assessment, platform selection, and portfolio diversification remain critical.

What's the difference between staking and crypto savings accounts?

Staking involves locking specific proof-of-stake cryptocurrencies to help validate blockchain transactions, earning rewards in return. Crypto savings accounts are broader products that may use staking as one yield-generation method among many, including lending, liquidity provision, and DeFi protocol participation. Savings accounts typically offer more flexibility and may provide yield on assets that can't be directly staked.

How much should I put in a crypto savings account?

Financial advisors generally recommend limiting crypto exposure to an amount you can afford to lose, often suggested as 5-15% of investable assets for those comfortable with higher risk. Within that crypto allocation, savings accounts can be appropriate for funds you don't need for active trading. Never deposit emergency funds or money you'll need short-term into crypto savings accounts, regardless of the yield offered.

Start earning higher yields today

The crypto savings landscape has evolved, offering investors more secure, transparent, and user-friendly options than before. While risks remain, choosing the right platform dramatically improves your risk-adjusted returns.

Pistachio.fi addresses the traditional barriers that have kept many investors from accessing crypto yield:

Curated Investment Vaults remove the complexity of evaluating hundreds of protocols

Expert Risk Grades on every option help you match investments to your comfort level

Completely Gasless transactions mean zero fees eating into your returns

Awaken.Tax Integration provides one-click tax export for stress-free compliance

Elite Security with institutional-grade custody protects your assets

Whether you're exploring crypto savings for the first time or optimizing an existing strategy, the platform you choose makes all the difference.

Related reading

Ready to put your crypto to work?

Visit Pistachio.fi to explore curated yield opportunities with institutional-grade security and zero transaction fees. Your journey to smarter crypto savings starts with a single click.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Cryptocurrency investments carry significant risks including potential loss of principal. Past performance does not guarantee future results. Always conduct your own research and consider consulting a financial advisor before making investment decisions.

Cross-chain crypto swaps: how Li.Fi powers Pistachio's one-tap zaps (2026)

Etherfuse stablebonds: earn government bond yields on-chain (2026)

How to earn money online in 2026 (crypto yield vs. the rest)

Linea crypto explained: what it is and how it works (2026)

Ethereum wallet guide 2026 (ethernet wallet explained)

DeFi Staking with Stader Labs: How ETHx Works in 2026

High-liquidity crypto exchanges: PancakeSwap guide 2026

What is Raydium? How Solana's AMM Works in 2026

Passive Income Ideas for 2026: 10 Ways That Actually Work

Hong Kong crypto news 2026: licenses, stablecoins, and regulation

©2026 Copyright, PistachioFi Inc.

©2026 Copyright, PistachioFi Inc.

©2026 Copyright, PistachioFi Inc.