Best Stablecoin Yield 2026: Earn 4–12% APY on USDC & USDT

Best Stablecoin Yield 2026: Earn 4–12% APY on USDC & USDT

Best Stablecoin Yield 2026: Earn 4–12% APY on USDC & USDT

Best Stablecoin Yield 2026: Earn 4–12% APY on USDC & USDT

Published: March 1, 2026 | Author: Pistachio Team

TL;DR

Stablecoins now earn more than most savings accounts, with DeFi lending rates for USDC and USDT sitting between 4% and 12% APY depending on platform and strategy. The safest yields come from battle-tested protocols like Aave (4–7%) and Curve (4–12% on stablecoin pools), while centralized options push higher but carry custodial risk. Pistachio.fi curates these vaults with expert risk grades so you can earn without spending hours comparing smart contracts.

Key takeaways

DeFi stablecoin yields in 2026 range from 2% on conservative protocols to 12%+ on higher-risk pools

Aave, Morpho, and Curve offer the best combination of security and competitive APY for USDC and USDT

Risk comes in three main forms: smart contract risk, counterparty risk, and peg risk. Each platform scores differently on each.

On-chain transactions with gasless wallets make stablecoin vaults far more accessible than they were two years ago

Tax reporting on stablecoin yield is mandatory in most jurisdictions. Pistachio integrates with Awaken.Tax to automate this.

Your USDC sitting in a standard wallet earns 0%. Meanwhile, the same USDC deposited into an Aave vault earns 4–7% APY right now. That gap has been true for years. Most people just haven't acted on it.

This guide covers where stablecoin yield actually comes from in 2026, which platforms offer the best returns at different risk levels, and how to evaluate what you're putting your money into before depositing.

Where stablecoin yield comes from

There are three main mechanisms generating stablecoin returns in DeFi today.

Lending protocols like Aave let you deposit USDC or USDT into a pool. Borrowers draw from that pool and pay interest. That interest, minus protocol fees, goes to depositors. Aave currently holds over $26 billion in TVL across its markets, making it the largest and most battle-tested lending protocol in DeFi. Its stablecoin rates fluctuate with borrowing demand but have consistently held in the 4–7% APY range through 2025 and into 2026.

Liquidity pools like those on Curve Finance earn fees from traders swapping between stablecoins. Because stablecoin swaps carry minimal price impact, Curve pools have developed a strong reputation for low-risk yield. The numbers reflect real activity rather than token emissions. Curve's stablecoin volume is dominated by organic swap demand, not incentive farming. Curve stablecoin pool yields typically land between 4% and 12% depending on the pool and incentive program.

Yield aggregators like Morpho sit one layer above, routing deposits across multiple protocols to capture the best available rate automatically. Morpho has grown significantly by offering optimized lending rates, often beating Aave's base rates by routing supply more efficiently.

2026 stablecoin yield comparison

Here's how the main platforms compare across the metrics that actually matter for stablecoin holders.

Platform | Stablecoin | APY Range | Yield Source | Risk Level |

|---|---|---|---|---|

Aave v3 | USDC, USDT, DAI | 4–7% | Lending interest | Low |

Morpho | USDC, USDT | 5–9% | Optimized lending | Low |

Curve Finance | USDC, USDT, DAI | 4–12% | Swap fees + CRV rewards | Low–Med |

Pendle (sUSDe) | sUSDe | 8–14% | Yield tokenization | Medium |

Nexo | USDC, USDT | Up to 16% | Centralized lending | High |

The 16% figure from centralized platforms looks good on paper. The risk calculus changes when you factor in that your funds are held by a third party with no on-chain transparency, counterparty exposure to their lending book, and no smart contract audit protecting your principal. The 2022–2023 cycle wiped out several centralized yield platforms that promised similar returns.

How to read the risk

Not all stablecoin yield is equal, and the headline APY number tells you almost nothing about what you're actually signing up for. There are three risk vectors worth understanding.

Smart contract risk is the baseline for all DeFi. If the underlying code has a bug, funds can be drained. Protocols like Aave have been audited repeatedly by multiple security firms and have operated without a major exploit for years. That track record matters more than any single audit report. Newer protocols with high advertised APYs and limited audit history carry meaningfully more smart contract risk.

Counterparty risk applies mainly to centralized platforms. When you deposit USDC into a centralized exchange's yield product, you're trusting their business model, solvency, and custody practices. You don't have on-chain visibility into where your funds are deployed.

Peg risk is specific to the stablecoin itself. USDC and USDT have the strongest peg histories, backed by large issuers with regular attestations. Algorithmic stablecoins (like the previous generation of UST-style tokens) carry the risk of a de-peg that could wipe out principal, not just yield. Any vault holding algorithmic stablecoins warrants extra scrutiny.

Pistachio assigns an expert risk grade to every vault in its platform, so you're not doing this analysis yourself for every strategy you consider. That grade reflects smart contract maturity, underlying stablecoin peg quality, TVL depth, and audit history, all condensed into a rating you can act on. Learn more about our approach in the Pistachio security overview.

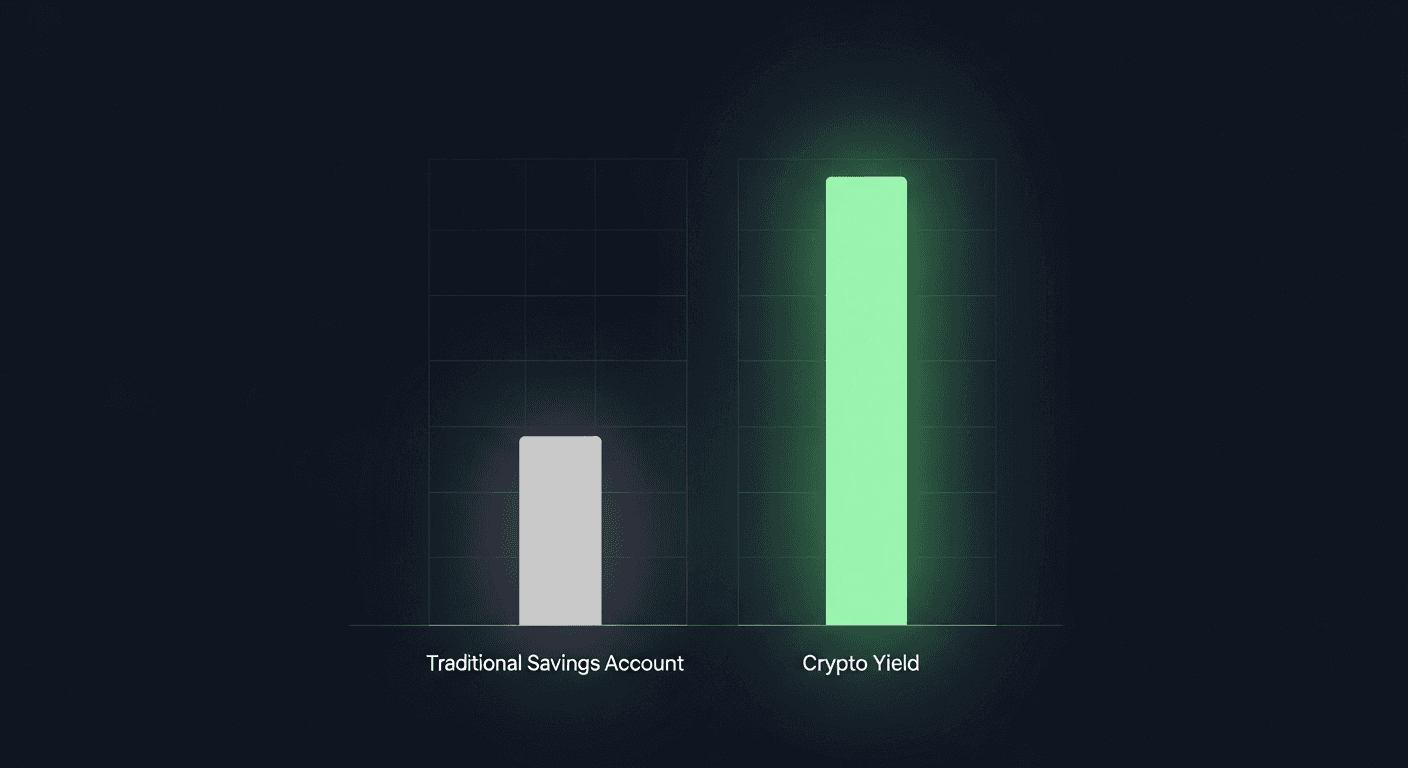

Stablecoin yield vs. traditional savings

US Treasury bill yields sat around 3.5% in late February 2026. High-yield savings accounts from major banks cluster around that same range. The best DeFi stablecoin rates on established protocols comfortably beat that benchmark while staying within protocols that have demonstrated years of reliable operation.

That's not an argument to put all your savings into DeFi. Traditional savings are federally insured. DeFi is not. But for risk capital you're already holding in crypto, the comparison matters. A USDC balance earning 0% in a wallet is a direct opportunity cost against the same balance earning 5–7% in Aave.

If you want a side-by-side breakdown including treasury yields, CETES, and traditional alternatives, our crypto vs. treasury yield 2026 article covers that comparison in detail.

Getting started without the complexity

The friction in stablecoin yield has historically been the gas fees. Depositing into Aave, Curve, or Morpho required Ethereum gas for every transaction. At peak network congestion, a deposit could cost $30–80 just to execute. That math doesn't work for smaller balances.

Pistachio operates as a smart account that handles gas internally, meaning you deposit your stablecoins and access vaults without paying Ethereum gas out of pocket. It's one of the changes that makes DeFi yield actually practical for amounts below $50,000. The user experience has caught up to the returns.

For an overview of passive income strategies beyond stablecoin yield, including ETH staking and liquidity provision, see our passive income crypto 2026 guide.

Tax on stablecoin yield: what you need to know

In most jurisdictions, yield earned from DeFi lending is taxable as ordinary income in the year you receive it. Every Aave interest accrual, every Curve fee distribution is a taxable event under IRS guidance and similar frameworks in the EU, UK, and Australia.

This is where most people get tripped up. The yield is real, the tax exposure is real, and manually tracking hundreds of micro-distributions across multiple protocols is a nightmare. Pistachio integrates with Awaken.Tax to automate this, pulling transaction data directly from your smart account and generating the reports your accountant actually needs.

For anyone earning meaningful yield across multiple vaults, the tax integration alone is worth more than the fee savings on gas. Crypto tax software without the on-chain integration is just another reconciliation headache.

What to watch in 2026

Stablecoin regulation is moving faster than most holders expect. The US GENIUS Act (signed into law in July 2025) and EU MiCA framework are both creating regulatory clarity around stablecoin issuers, which should reduce peg risk for the major coins over time. More regulated issuers means more verifiable reserves, which means less uncertainty in the stablecoins underlying these yield strategies.

At the same time, yield from token emissions (where protocols pay out newly minted governance tokens as rewards) is compressing as token prices stabilize. The sustainable yield in 2026 increasingly comes from real protocol revenue: borrowing interest, swap fees, protocol usage. That's a healthy development. It means the 4–7% ranges on established protocols reflect actual economic activity, not inflationary rewards that dilute over time.

Earn stablecoin yield without the complexity

Pistachio curates the best DeFi vaults, assigns risk grades to every strategy, and handles gas so you don't have to.

Start earning on Pistachio.fi →

Frequently asked questions

What is the best stablecoin to earn yield on in 2026?

USDC and USDT are the strongest options for most holders. Both have large on-chain liquidity, deep Aave and Curve market support, and the longest track records of maintaining their peg. DAI is a solid choice in Curve pools. Avoid algorithmic stablecoins or synthetic dollar tokens unless you've done significant due diligence on the underlying mechanism.

Is DeFi stablecoin yield safe?

Battle-tested protocols like Aave v3 and Curve carry low smart contract risk given their years of operation and repeated audits, but "safe" is relative. There's no FDIC insurance for DeFi deposits, and smart contract bugs, protocol governance attacks, and stablecoin de-pegs are real risks. Sticking to protocols with billions in TVL and multi-year track records significantly reduces exposure.

How does Pistachio.fi earn stablecoin yield?

Pistachio routes your stablecoins into curated DeFi vaults, primarily on protocols like Aave and Morpho, and assigns each vault an expert risk grade. The platform handles gas through its smart account infrastructure, so you don't pay Ethereum transaction fees out of pocket. Your funds remain in on-chain protocols, not held custodially by Pistachio.

Do I owe taxes on stablecoin yield?

Yes, in most jurisdictions. Yield earned from DeFi lending protocols is typically classified as ordinary income. Pistachio integrates with Awaken.Tax to track your earnings and generate the documentation you need for tax reporting. You should also consult a qualified crypto tax professional for guidance specific to your situation.

What APY is realistic for stablecoin yield in 2026?

For low-risk DeFi strategies on established protocols, 4–7% APY is a realistic and sustainable expectation. Curve pools with additional incentives can reach 8–12%. Anything above 12% on stablecoins generally involves either centralized counterparty risk, newer protocols with limited track records, or synthetic yield mechanisms with more complexity. The T-bill rate of ~3.5% is a useful baseline: any DeFi yield above that should have a clear explanation for why the premium exists.

External resources

DefiLlama Stablecoin Yields — real-time APY data across protocols

Aave Protocol — current lending rates for USDC, USDT, DAI

Curve Finance — stablecoin pool rates and TVL data

Published: March 1, 2026 | Author: Pistachio Team

TL;DR

Stablecoins now earn more than most savings accounts, with DeFi lending rates for USDC and USDT sitting between 4% and 12% APY depending on platform and strategy. The safest yields come from battle-tested protocols like Aave (4–7%) and Curve (4–12% on stablecoin pools), while centralized options push higher but carry custodial risk. Pistachio.fi curates these vaults with expert risk grades so you can earn without spending hours comparing smart contracts.

Key takeaways

DeFi stablecoin yields in 2026 range from 2% on conservative protocols to 12%+ on higher-risk pools

Aave, Morpho, and Curve offer the best combination of security and competitive APY for USDC and USDT

Risk comes in three main forms: smart contract risk, counterparty risk, and peg risk. Each platform scores differently on each.

On-chain transactions with gasless wallets make stablecoin vaults far more accessible than they were two years ago

Tax reporting on stablecoin yield is mandatory in most jurisdictions. Pistachio integrates with Awaken.Tax to automate this.

Your USDC sitting in a standard wallet earns 0%. Meanwhile, the same USDC deposited into an Aave vault earns 4–7% APY right now. That gap has been true for years. Most people just haven't acted on it.

This guide covers where stablecoin yield actually comes from in 2026, which platforms offer the best returns at different risk levels, and how to evaluate what you're putting your money into before depositing.

Where stablecoin yield comes from

There are three main mechanisms generating stablecoin returns in DeFi today.

Lending protocols like Aave let you deposit USDC or USDT into a pool. Borrowers draw from that pool and pay interest. That interest, minus protocol fees, goes to depositors. Aave currently holds over $26 billion in TVL across its markets, making it the largest and most battle-tested lending protocol in DeFi. Its stablecoin rates fluctuate with borrowing demand but have consistently held in the 4–7% APY range through 2025 and into 2026.

Liquidity pools like those on Curve Finance earn fees from traders swapping between stablecoins. Because stablecoin swaps carry minimal price impact, Curve pools have developed a strong reputation for low-risk yield. The numbers reflect real activity rather than token emissions. Curve's stablecoin volume is dominated by organic swap demand, not incentive farming. Curve stablecoin pool yields typically land between 4% and 12% depending on the pool and incentive program.

Yield aggregators like Morpho sit one layer above, routing deposits across multiple protocols to capture the best available rate automatically. Morpho has grown significantly by offering optimized lending rates, often beating Aave's base rates by routing supply more efficiently.

2026 stablecoin yield comparison

Here's how the main platforms compare across the metrics that actually matter for stablecoin holders.

Platform | Stablecoin | APY Range | Yield Source | Risk Level |

|---|---|---|---|---|

Aave v3 | USDC, USDT, DAI | 4–7% | Lending interest | Low |

Morpho | USDC, USDT | 5–9% | Optimized lending | Low |

Curve Finance | USDC, USDT, DAI | 4–12% | Swap fees + CRV rewards | Low–Med |

Pendle (sUSDe) | sUSDe | 8–14% | Yield tokenization | Medium |

Nexo | USDC, USDT | Up to 16% | Centralized lending | High |

The 16% figure from centralized platforms looks good on paper. The risk calculus changes when you factor in that your funds are held by a third party with no on-chain transparency, counterparty exposure to their lending book, and no smart contract audit protecting your principal. The 2022–2023 cycle wiped out several centralized yield platforms that promised similar returns.

How to read the risk

Not all stablecoin yield is equal, and the headline APY number tells you almost nothing about what you're actually signing up for. There are three risk vectors worth understanding.

Smart contract risk is the baseline for all DeFi. If the underlying code has a bug, funds can be drained. Protocols like Aave have been audited repeatedly by multiple security firms and have operated without a major exploit for years. That track record matters more than any single audit report. Newer protocols with high advertised APYs and limited audit history carry meaningfully more smart contract risk.

Counterparty risk applies mainly to centralized platforms. When you deposit USDC into a centralized exchange's yield product, you're trusting their business model, solvency, and custody practices. You don't have on-chain visibility into where your funds are deployed.

Peg risk is specific to the stablecoin itself. USDC and USDT have the strongest peg histories, backed by large issuers with regular attestations. Algorithmic stablecoins (like the previous generation of UST-style tokens) carry the risk of a de-peg that could wipe out principal, not just yield. Any vault holding algorithmic stablecoins warrants extra scrutiny.

Pistachio assigns an expert risk grade to every vault in its platform, so you're not doing this analysis yourself for every strategy you consider. That grade reflects smart contract maturity, underlying stablecoin peg quality, TVL depth, and audit history, all condensed into a rating you can act on. Learn more about our approach in the Pistachio security overview.

Stablecoin yield vs. traditional savings

US Treasury bill yields sat around 3.5% in late February 2026. High-yield savings accounts from major banks cluster around that same range. The best DeFi stablecoin rates on established protocols comfortably beat that benchmark while staying within protocols that have demonstrated years of reliable operation.

That's not an argument to put all your savings into DeFi. Traditional savings are federally insured. DeFi is not. But for risk capital you're already holding in crypto, the comparison matters. A USDC balance earning 0% in a wallet is a direct opportunity cost against the same balance earning 5–7% in Aave.

If you want a side-by-side breakdown including treasury yields, CETES, and traditional alternatives, our crypto vs. treasury yield 2026 article covers that comparison in detail.

Getting started without the complexity

The friction in stablecoin yield has historically been the gas fees. Depositing into Aave, Curve, or Morpho required Ethereum gas for every transaction. At peak network congestion, a deposit could cost $30–80 just to execute. That math doesn't work for smaller balances.

Pistachio operates as a smart account that handles gas internally, meaning you deposit your stablecoins and access vaults without paying Ethereum gas out of pocket. It's one of the changes that makes DeFi yield actually practical for amounts below $50,000. The user experience has caught up to the returns.

For an overview of passive income strategies beyond stablecoin yield, including ETH staking and liquidity provision, see our passive income crypto 2026 guide.

Tax on stablecoin yield: what you need to know

In most jurisdictions, yield earned from DeFi lending is taxable as ordinary income in the year you receive it. Every Aave interest accrual, every Curve fee distribution is a taxable event under IRS guidance and similar frameworks in the EU, UK, and Australia.

This is where most people get tripped up. The yield is real, the tax exposure is real, and manually tracking hundreds of micro-distributions across multiple protocols is a nightmare. Pistachio integrates with Awaken.Tax to automate this, pulling transaction data directly from your smart account and generating the reports your accountant actually needs.

For anyone earning meaningful yield across multiple vaults, the tax integration alone is worth more than the fee savings on gas. Crypto tax software without the on-chain integration is just another reconciliation headache.

What to watch in 2026

Stablecoin regulation is moving faster than most holders expect. The US GENIUS Act (signed into law in July 2025) and EU MiCA framework are both creating regulatory clarity around stablecoin issuers, which should reduce peg risk for the major coins over time. More regulated issuers means more verifiable reserves, which means less uncertainty in the stablecoins underlying these yield strategies.

At the same time, yield from token emissions (where protocols pay out newly minted governance tokens as rewards) is compressing as token prices stabilize. The sustainable yield in 2026 increasingly comes from real protocol revenue: borrowing interest, swap fees, protocol usage. That's a healthy development. It means the 4–7% ranges on established protocols reflect actual economic activity, not inflationary rewards that dilute over time.

Earn stablecoin yield without the complexity

Pistachio curates the best DeFi vaults, assigns risk grades to every strategy, and handles gas so you don't have to.

Start earning on Pistachio.fi →

Frequently asked questions

What is the best stablecoin to earn yield on in 2026?

USDC and USDT are the strongest options for most holders. Both have large on-chain liquidity, deep Aave and Curve market support, and the longest track records of maintaining their peg. DAI is a solid choice in Curve pools. Avoid algorithmic stablecoins or synthetic dollar tokens unless you've done significant due diligence on the underlying mechanism.

Is DeFi stablecoin yield safe?

Battle-tested protocols like Aave v3 and Curve carry low smart contract risk given their years of operation and repeated audits, but "safe" is relative. There's no FDIC insurance for DeFi deposits, and smart contract bugs, protocol governance attacks, and stablecoin de-pegs are real risks. Sticking to protocols with billions in TVL and multi-year track records significantly reduces exposure.

How does Pistachio.fi earn stablecoin yield?

Pistachio routes your stablecoins into curated DeFi vaults, primarily on protocols like Aave and Morpho, and assigns each vault an expert risk grade. The platform handles gas through its smart account infrastructure, so you don't pay Ethereum transaction fees out of pocket. Your funds remain in on-chain protocols, not held custodially by Pistachio.

Do I owe taxes on stablecoin yield?

Yes, in most jurisdictions. Yield earned from DeFi lending protocols is typically classified as ordinary income. Pistachio integrates with Awaken.Tax to track your earnings and generate the documentation you need for tax reporting. You should also consult a qualified crypto tax professional for guidance specific to your situation.

What APY is realistic for stablecoin yield in 2026?

For low-risk DeFi strategies on established protocols, 4–7% APY is a realistic and sustainable expectation. Curve pools with additional incentives can reach 8–12%. Anything above 12% on stablecoins generally involves either centralized counterparty risk, newer protocols with limited track records, or synthetic yield mechanisms with more complexity. The T-bill rate of ~3.5% is a useful baseline: any DeFi yield above that should have a clear explanation for why the premium exists.

External resources

DefiLlama Stablecoin Yields — real-time APY data across protocols

Aave Protocol — current lending rates for USDC, USDT, DAI

Curve Finance — stablecoin pool rates and TVL data

Cross-chain crypto swaps: how Li.Fi powers Pistachio's one-tap zaps (2026)

Etherfuse stablebonds: earn government bond yields on-chain (2026)

How to earn money online in 2026 (crypto yield vs. the rest)

Linea crypto explained: what it is and how it works (2026)

Ethereum wallet guide 2026 (ethernet wallet explained)

DeFi Staking with Stader Labs: How ETHx Works in 2026

High-liquidity crypto exchanges: PancakeSwap guide 2026

What is Raydium? How Solana's AMM Works in 2026

Passive Income Ideas for 2026: 10 Ways That Actually Work

Hong Kong crypto news 2026: licenses, stablecoins, and regulation

©2026 Copyright, PistachioFi Inc.

©2026 Copyright, PistachioFi Inc.

©2026 Copyright, PistachioFi Inc.