How to earn money online in 2026 (crypto yield vs. the rest)

How to earn money online in 2026 (crypto yield vs. the rest)

How to earn money online in 2026 (crypto yield vs. the rest)

How to earn money online in 2026 (crypto yield vs. the rest)

Last updated: March 2026

Most content about earning money online pushes the same playbook: start freelancing, launch a YouTube channel, sell courses, take surveys. All of those work to varying degrees. But there's a category that rarely gets a fair hearing in these conversations: crypto yield.

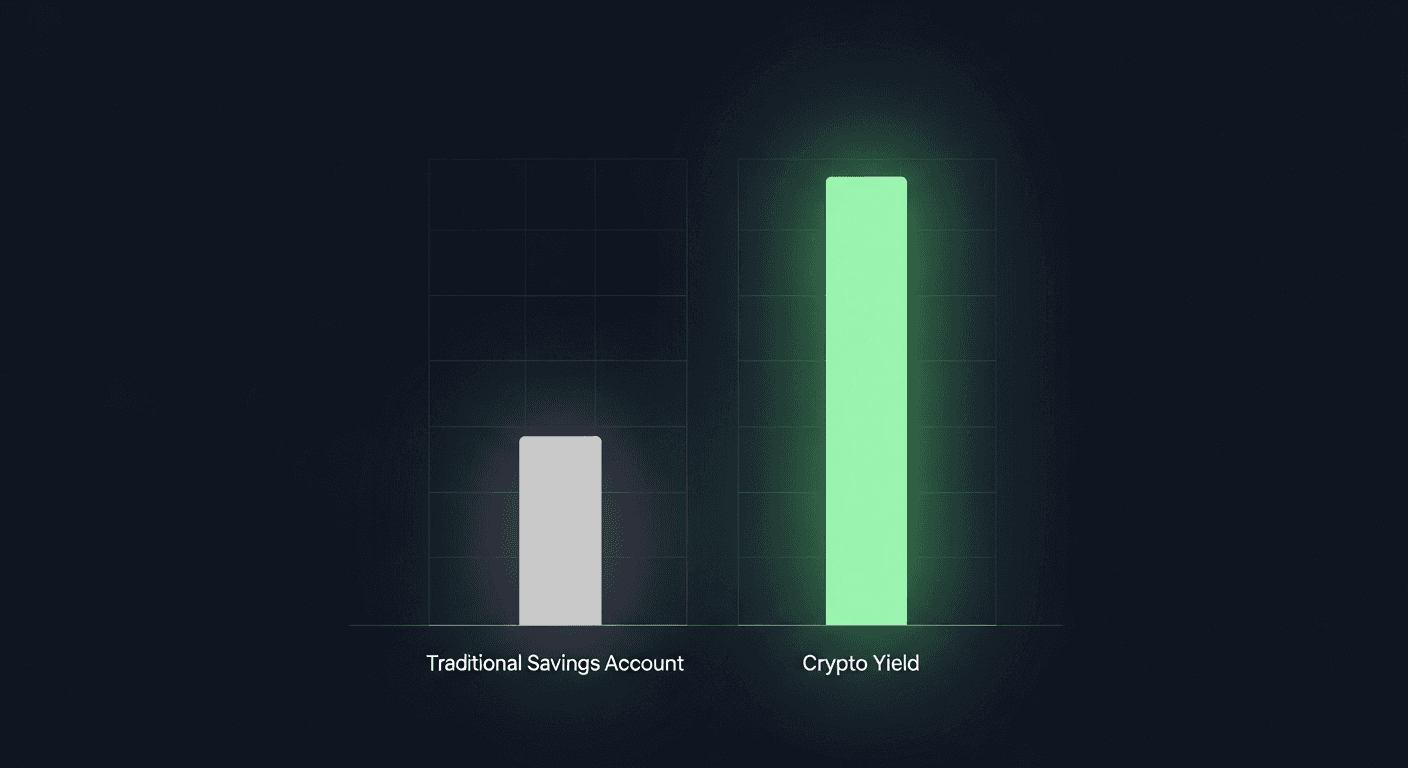

The pitch is straightforward. You hold savings. Those savings sit in an account earning 0.61% annually (the US national average, per Bankrate's March 2026 data). Meanwhile, Ethereum-based lending protocols are paying 4-10% on stablecoins and 3-4% on staked ETH, continuously, with no ongoing labor.

This article covers both the traditional and crypto-based approaches to earning online, what each actually requires, and where the numbers genuinely stack up in 2026.

Earning money online in 2026 spans a wide range, from active income like freelancing and content creation to genuinely passive strategies like crypto yield. For passive income, Ethereum-based lending and staking protocols offer 3-10% APY on crypto assets, compared to a national average of 0.61% from traditional savings accounts (Bankrate, March 2026). DeFi protocols with long track records and external risk oversight offer a reasonable entry point for anyone treating savings as productive capital. Evaluate platforms by audit history, yield source transparency, and whether the protocol has operated without losses through previous market cycles before depositing.

Key takeaways

Crypto yield is one of the few genuinely passive ways to earn money online, requiring no ongoing work after setup

Current returns: ETH staking yields around 3-4% APY; USDC lending ranges 4-10% APY, vs. 0.61% from the average US savings account

DeFi TVL reached $105 billion in early 2026, with 25.3 million ETH deployed across protocols (CoinDesk, Feb 2026)

Smart contract risk exists: choosing audited protocols with multi-year track records and active risk management reduces exposure

Getting started takes under 10 minutes on platforms that handle gas fees and provide built-in wallets

What "earn money online" actually covers in 2026

The phrase gets thrown at very different categories of income. Worth separating them clearly:

Active income trades time directly for money. Freelancing, virtual assistance, gig work. You stop working, the income stops. According to Pew Research, roughly 1 in 4 Americans already earn income this way through online platforms.

Semi-passive income front-loads effort for later payoff. YouTube channels, newsletters, affiliate sites, digital products. Most require 12-18 months before generating meaningful returns. The creator economy is large (50+ million creators estimated globally), but income distribution is brutal: only 4.3% of creators earn over $100k annually.

Passive income earns without ongoing work. Dividend stocks, interest on savings, real estate income, crypto yield. The capital does the work. The practical barrier is that you need capital to start.

This guide focuses on the passive category, specifically what's changed in crypto yield that makes it worth reconsidering for anyone who's previously dismissed it.

How does crypto yield compare to alternatives?

The comparison that matters most is simple. High-yield savings accounts in the US offer up to 5% APY from the best providers, with the category average at 1.64% and the national overall average at 0.61%. Dividend stocks average 2-4% annually with market-rate volatility. Against that backdrop:

Method | Typical annual yield | Work required | Liquidity |

|---|---|---|---|

Traditional savings (national avg) | 0.61% | None | High |

High-yield savings (top tier) | 4.5-5.0% | None | High |

Dividend stocks | 2-4% | Low (pick stocks) | High |

ETH liquid staking (Lido/Rocket Pool) | 3-4% APY | Low | Medium |

USDC lending (Compound, Morpho) | 4-10% APY | Low | High |

Curated DeFi vaults | 5-12% APY | Low (managed) | Medium |

The spread between top high-yield savings and on-chain yields has narrowed as rate environments shift, but there's still a meaningful gap at the higher end of DeFi. That gap exists because crypto protocols price yields based on real borrowing demand rather than bank profit margins.

How does crypto yield actually work?

Three mechanisms drive most of the yield in this space:

Staking secures the Ethereum network. Validators lock ETH, process transactions, and earn protocol rewards in return (currently around 3-4% annually). You don't need 32 ETH to participate. Liquid staking protocols like Lido pool deposits, so any amount earns staking rewards. You deposit ETH and receive stETH, a token that accrues yield automatically.

Lending works like a bank, but on public rails. You deposit stablecoins (like USDC) or crypto assets that other users borrow against collateral. You earn the interest those borrowers pay. Compound is one of the oldest protocols doing this, with an uninterrupted track record dating to 2018. Morpho optimizes lending further by matching lenders and borrowers directly when possible, typically delivering better rates than pooled lending alone.

Curated vaults bundle strategies across protocols. Rather than depositing to a single market and monitoring it yourself, a vault allocates dynamically across lending markets to capture the best available rate. Gauntlet, a quantitative risk management firm, actively manages vault allocations on Morpho to balance yield against exposure risk.

All three require no ongoing input after the initial deposit. That's the core appeal for anyone treating this as passive income.

Is the DeFi infrastructure actually reliable now?

This is the right question to ask, especially given 2022-2023 events. The Luna/UST collapse, Celsius freezing withdrawals, and several high-profile exploits caused real damage to people who treated DeFi as equivalent to a savings account.

The protocols that survived that period have now operated through multiple market cycles. Compound has been running since 2018 without a major loss event. Morpho launched in 2022 and processed billions in lending volume without a hack. Lido holds roughly 30% of all staked ETH with no slashing incidents at scale.

That said, calling any DeFi protocol "safe" in an absolute sense isn't accurate. Smart contract bugs remain a real vector. Protocol governance can make mistakes. Stablecoin pegs can break under stress. The question is risk-adjusted return, not zero risk.

What's improved is the quality of risk infrastructure around these protocols. External risk managers like Gauntlet actively manage vault parameters and exposure limits. Audit firms publish findings publicly. Users can review track records rather than relying on marketing.

Where platforms like Pistachio.fi fit in

The gap between "DeFi is interesting" and "I have money working in DeFi" used to be filled with wallet setup friction, gas fee confusion, and having to evaluate protocols yourself.

Pistachio.fi is a mobile app that removes most of that friction. You create a self-custodial wallet directly inside the app, so there's no separate browser extension to install or seed phrase to manage from day one. The app provides access to pre-screened vaults including Gauntlet (on Morpho), IPOR, YO.xyz, Etherfuse, and Compound, each with expert risk grades so users know what they're taking on before depositing.

The gasless part matters more than it sounds. On Ethereum in 2026, most transactions cost under $0.25. But when you're managing yield positions, you're executing multiple transactions over time: deposits, withdrawals, vault switches. Pistachio covers all gas fees, which simplifies the math. You see yield in, not yield in minus gas out.

For tax purposes, Pistachio integrates with Awaken.Tax for one-tap portfolio export. Crypto yield is generally taxable as ordinary income in most jurisdictions, and keeping clean records is non-negotiable.

US users can deposit with Apple Pay at no fee. The app supports fiat onramps through Coinbase Ramp and Onramper across 130+ countries.

Active ways to earn money online in 2026

Crypto yield is one answer. Here's an honest look at the rest of the field:

Freelancing remains the most accessible starting point. Platforms like Upwork and Fiverr have seen demand shift toward AI-adjacent skills: prompt engineering, model fine-tuning, AI content editing, and workflow automation. Commodity tasks face intense competition. Specialized skills command real rates.

Content creation has a long ramp. The channels earning meaningfully in 2026 are generally either very niche (serving an audience nobody else is targeting) or have exceptional production quality. Monetization takes time; plan for 12-18 months of consistent output before income is meaningful.

Digital products scale well once built. Courses, templates, and tools can sell without proportional effort, but they require genuine expertise and marketing to find buyers. The "build it and they'll come" model doesn't work.

Affiliate marketing still generates income for the right audience and topic, but algorithm changes have made generic comparison content increasingly hard to rank or trust. The people doing well are those with authentic domain knowledge.

The honest comparison: passive crypto yield doesn't require skill development, audience building, or a product. It requires capital and a reasonable risk assessment. Active methods don't require capital but do require sustained time and effort.

What are the real risks of crypto yield?

Smart contract risk is the primary one. A bug in protocol code could theoretically allow an attacker to drain funds. Using audited protocols with long operating histories reduces but doesn't eliminate this. The Pistachio security overview covers how vault selection accounts for audit status and track record.

Market risk matters if you hold ETH rather than stablecoins. ETH staking yields 3-4%, but if ETH drops 20%, the dollar value of your position drops even while yield accumulates. Stablecoin lending removes price exposure; your principal stays in USDC.

Counterparty and protocol risk means a protocol could have governance failures, accumulate bad debt, or face liquidity issues. Active risk managers like Gauntlet monitor and adjust vault parameters to limit this exposure.

Regulatory risk varies by jurisdiction. In the US, the GENIUS Act (passed in 2025) established clearer treatment for stablecoins, which is positive context. Yield earned on crypto is generally taxable as income in the year received. Tax reporting tools make compliance straightforward; ignoring it doesn't.

How to get started with crypto yield

The practical steps, with Pistachio as the example:

Download the app and create your wallet. The wallet is created inside Pistachio, so there's no external setup required. You own the keys.

Fund with fiat or crypto. US users can deposit via Apple Pay (no fee). International users can use Coinbase Ramp or Onramper in 130+ countries. Alternatively, transfer existing crypto directly.

Pick a vault. Browse by yield and risk grade. Lower-risk vaults concentrate in larger, audited protocols. Higher-yield vaults take on more protocol diversity. Choose based on your comfort with each risk rating.

Deposit and earn. The app handles gas fees. Yield accrues to your balance continuously. Withdraw anytime.

For a broader view of how these vaults rank against alternatives, the best crypto yield platforms 2026 comparison covers protocol-level differences in more detail. If you're new to the self-custody concept, Pistachio's security overview explains how custody works in practice. And for a deeper look at ETH staking specifically, the Ethereum staking yield guide covers the mechanics.

Start earning yield on your crypto

Pistachio gives you access to curated DeFi vaults with expert risk grades, zero gas fees, and a built-in self-custodial wallet. No DeFi expertise required.

Frequently asked questions

Can you really earn passive income online with crypto in 2026?

Yes. ETH staking and stablecoin lending generate continuous yield with no ongoing labor after the initial deposit. Current rates: ETH liquid staking around 3-4% APY via protocols like Lido, USDC lending 4-10% APY on platforms like Compound and Morpho depending on current demand. Yields fluctuate with market conditions and aren't guaranteed, but the underlying mechanism, lending to over-collateralized borrowers on audited protocols, is real and operational at scale.

How much money do you need to start earning crypto yield online?

There's no technical minimum. Compound and Morpho accept any deposit size. Practically speaking, a few hundred dollars is where the yield becomes meaningfully visible relative to gas costs (though Pistachio covers those fees entirely for its users). At $1,000 deposited and 6% APY, you'd earn roughly $60 in a year, paid continuously without any additional input.

Is DeFi yield income taxable?

In the US and most jurisdictions, yes. Yield earned on crypto lending or staking is generally treated as ordinary income at the time it's received, similar to bank interest. The dollar value at the time of receipt is what's reportable. Pistachio integrates with Awaken.Tax for one-tap portfolio export, which simplifies the record-keeping significantly.

What's the difference between ETH staking and stablecoin lending?

Both earn yield, but they carry different risk profiles. ETH staking earns 3-4% APY but your principal is in ETH, which moves with crypto markets. If ETH drops 20%, your dollar value drops even while yield accrues. Stablecoin lending keeps your principal in USDC (pegged to $1) and earns 4-10% APY, so you're earning yield without taking on crypto price exposure. Stablecoin lending carries stablecoin peg risk and protocol smart contract risk, but no ETH price risk.

How is earning money online with crypto different from trading?

Trading involves actively buying and selling assets to profit from price movements. It requires time, analysis, and skill, and most retail traders lose money relative to simply holding. Crypto yield is passive: you deposit assets into a lending protocol or staking mechanism and earn interest, with no active management required. The return profile is also different: yield is steady and predictable (within normal rate ranges), while trading profits are highly variable.

Last updated: March 2026

Most content about earning money online pushes the same playbook: start freelancing, launch a YouTube channel, sell courses, take surveys. All of those work to varying degrees. But there's a category that rarely gets a fair hearing in these conversations: crypto yield.

The pitch is straightforward. You hold savings. Those savings sit in an account earning 0.61% annually (the US national average, per Bankrate's March 2026 data). Meanwhile, Ethereum-based lending protocols are paying 4-10% on stablecoins and 3-4% on staked ETH, continuously, with no ongoing labor.

This article covers both the traditional and crypto-based approaches to earning online, what each actually requires, and where the numbers genuinely stack up in 2026.

Earning money online in 2026 spans a wide range, from active income like freelancing and content creation to genuinely passive strategies like crypto yield. For passive income, Ethereum-based lending and staking protocols offer 3-10% APY on crypto assets, compared to a national average of 0.61% from traditional savings accounts (Bankrate, March 2026). DeFi protocols with long track records and external risk oversight offer a reasonable entry point for anyone treating savings as productive capital. Evaluate platforms by audit history, yield source transparency, and whether the protocol has operated without losses through previous market cycles before depositing.

Key takeaways

Crypto yield is one of the few genuinely passive ways to earn money online, requiring no ongoing work after setup

Current returns: ETH staking yields around 3-4% APY; USDC lending ranges 4-10% APY, vs. 0.61% from the average US savings account

DeFi TVL reached $105 billion in early 2026, with 25.3 million ETH deployed across protocols (CoinDesk, Feb 2026)

Smart contract risk exists: choosing audited protocols with multi-year track records and active risk management reduces exposure

Getting started takes under 10 minutes on platforms that handle gas fees and provide built-in wallets

What "earn money online" actually covers in 2026

The phrase gets thrown at very different categories of income. Worth separating them clearly:

Active income trades time directly for money. Freelancing, virtual assistance, gig work. You stop working, the income stops. According to Pew Research, roughly 1 in 4 Americans already earn income this way through online platforms.

Semi-passive income front-loads effort for later payoff. YouTube channels, newsletters, affiliate sites, digital products. Most require 12-18 months before generating meaningful returns. The creator economy is large (50+ million creators estimated globally), but income distribution is brutal: only 4.3% of creators earn over $100k annually.

Passive income earns without ongoing work. Dividend stocks, interest on savings, real estate income, crypto yield. The capital does the work. The practical barrier is that you need capital to start.

This guide focuses on the passive category, specifically what's changed in crypto yield that makes it worth reconsidering for anyone who's previously dismissed it.

How does crypto yield compare to alternatives?

The comparison that matters most is simple. High-yield savings accounts in the US offer up to 5% APY from the best providers, with the category average at 1.64% and the national overall average at 0.61%. Dividend stocks average 2-4% annually with market-rate volatility. Against that backdrop:

Method | Typical annual yield | Work required | Liquidity |

|---|---|---|---|

Traditional savings (national avg) | 0.61% | None | High |

High-yield savings (top tier) | 4.5-5.0% | None | High |

Dividend stocks | 2-4% | Low (pick stocks) | High |

ETH liquid staking (Lido/Rocket Pool) | 3-4% APY | Low | Medium |

USDC lending (Compound, Morpho) | 4-10% APY | Low | High |

Curated DeFi vaults | 5-12% APY | Low (managed) | Medium |

The spread between top high-yield savings and on-chain yields has narrowed as rate environments shift, but there's still a meaningful gap at the higher end of DeFi. That gap exists because crypto protocols price yields based on real borrowing demand rather than bank profit margins.

How does crypto yield actually work?

Three mechanisms drive most of the yield in this space:

Staking secures the Ethereum network. Validators lock ETH, process transactions, and earn protocol rewards in return (currently around 3-4% annually). You don't need 32 ETH to participate. Liquid staking protocols like Lido pool deposits, so any amount earns staking rewards. You deposit ETH and receive stETH, a token that accrues yield automatically.

Lending works like a bank, but on public rails. You deposit stablecoins (like USDC) or crypto assets that other users borrow against collateral. You earn the interest those borrowers pay. Compound is one of the oldest protocols doing this, with an uninterrupted track record dating to 2018. Morpho optimizes lending further by matching lenders and borrowers directly when possible, typically delivering better rates than pooled lending alone.

Curated vaults bundle strategies across protocols. Rather than depositing to a single market and monitoring it yourself, a vault allocates dynamically across lending markets to capture the best available rate. Gauntlet, a quantitative risk management firm, actively manages vault allocations on Morpho to balance yield against exposure risk.

All three require no ongoing input after the initial deposit. That's the core appeal for anyone treating this as passive income.

Is the DeFi infrastructure actually reliable now?

This is the right question to ask, especially given 2022-2023 events. The Luna/UST collapse, Celsius freezing withdrawals, and several high-profile exploits caused real damage to people who treated DeFi as equivalent to a savings account.

The protocols that survived that period have now operated through multiple market cycles. Compound has been running since 2018 without a major loss event. Morpho launched in 2022 and processed billions in lending volume without a hack. Lido holds roughly 30% of all staked ETH with no slashing incidents at scale.

That said, calling any DeFi protocol "safe" in an absolute sense isn't accurate. Smart contract bugs remain a real vector. Protocol governance can make mistakes. Stablecoin pegs can break under stress. The question is risk-adjusted return, not zero risk.

What's improved is the quality of risk infrastructure around these protocols. External risk managers like Gauntlet actively manage vault parameters and exposure limits. Audit firms publish findings publicly. Users can review track records rather than relying on marketing.

Where platforms like Pistachio.fi fit in

The gap between "DeFi is interesting" and "I have money working in DeFi" used to be filled with wallet setup friction, gas fee confusion, and having to evaluate protocols yourself.

Pistachio.fi is a mobile app that removes most of that friction. You create a self-custodial wallet directly inside the app, so there's no separate browser extension to install or seed phrase to manage from day one. The app provides access to pre-screened vaults including Gauntlet (on Morpho), IPOR, YO.xyz, Etherfuse, and Compound, each with expert risk grades so users know what they're taking on before depositing.

The gasless part matters more than it sounds. On Ethereum in 2026, most transactions cost under $0.25. But when you're managing yield positions, you're executing multiple transactions over time: deposits, withdrawals, vault switches. Pistachio covers all gas fees, which simplifies the math. You see yield in, not yield in minus gas out.

For tax purposes, Pistachio integrates with Awaken.Tax for one-tap portfolio export. Crypto yield is generally taxable as ordinary income in most jurisdictions, and keeping clean records is non-negotiable.

US users can deposit with Apple Pay at no fee. The app supports fiat onramps through Coinbase Ramp and Onramper across 130+ countries.

Active ways to earn money online in 2026

Crypto yield is one answer. Here's an honest look at the rest of the field:

Freelancing remains the most accessible starting point. Platforms like Upwork and Fiverr have seen demand shift toward AI-adjacent skills: prompt engineering, model fine-tuning, AI content editing, and workflow automation. Commodity tasks face intense competition. Specialized skills command real rates.

Content creation has a long ramp. The channels earning meaningfully in 2026 are generally either very niche (serving an audience nobody else is targeting) or have exceptional production quality. Monetization takes time; plan for 12-18 months of consistent output before income is meaningful.

Digital products scale well once built. Courses, templates, and tools can sell without proportional effort, but they require genuine expertise and marketing to find buyers. The "build it and they'll come" model doesn't work.

Affiliate marketing still generates income for the right audience and topic, but algorithm changes have made generic comparison content increasingly hard to rank or trust. The people doing well are those with authentic domain knowledge.

The honest comparison: passive crypto yield doesn't require skill development, audience building, or a product. It requires capital and a reasonable risk assessment. Active methods don't require capital but do require sustained time and effort.

What are the real risks of crypto yield?

Smart contract risk is the primary one. A bug in protocol code could theoretically allow an attacker to drain funds. Using audited protocols with long operating histories reduces but doesn't eliminate this. The Pistachio security overview covers how vault selection accounts for audit status and track record.

Market risk matters if you hold ETH rather than stablecoins. ETH staking yields 3-4%, but if ETH drops 20%, the dollar value of your position drops even while yield accumulates. Stablecoin lending removes price exposure; your principal stays in USDC.

Counterparty and protocol risk means a protocol could have governance failures, accumulate bad debt, or face liquidity issues. Active risk managers like Gauntlet monitor and adjust vault parameters to limit this exposure.

Regulatory risk varies by jurisdiction. In the US, the GENIUS Act (passed in 2025) established clearer treatment for stablecoins, which is positive context. Yield earned on crypto is generally taxable as income in the year received. Tax reporting tools make compliance straightforward; ignoring it doesn't.

How to get started with crypto yield

The practical steps, with Pistachio as the example:

Download the app and create your wallet. The wallet is created inside Pistachio, so there's no external setup required. You own the keys.

Fund with fiat or crypto. US users can deposit via Apple Pay (no fee). International users can use Coinbase Ramp or Onramper in 130+ countries. Alternatively, transfer existing crypto directly.

Pick a vault. Browse by yield and risk grade. Lower-risk vaults concentrate in larger, audited protocols. Higher-yield vaults take on more protocol diversity. Choose based on your comfort with each risk rating.

Deposit and earn. The app handles gas fees. Yield accrues to your balance continuously. Withdraw anytime.

For a broader view of how these vaults rank against alternatives, the best crypto yield platforms 2026 comparison covers protocol-level differences in more detail. If you're new to the self-custody concept, Pistachio's security overview explains how custody works in practice. And for a deeper look at ETH staking specifically, the Ethereum staking yield guide covers the mechanics.

Start earning yield on your crypto

Pistachio gives you access to curated DeFi vaults with expert risk grades, zero gas fees, and a built-in self-custodial wallet. No DeFi expertise required.

Frequently asked questions

Can you really earn passive income online with crypto in 2026?

Yes. ETH staking and stablecoin lending generate continuous yield with no ongoing labor after the initial deposit. Current rates: ETH liquid staking around 3-4% APY via protocols like Lido, USDC lending 4-10% APY on platforms like Compound and Morpho depending on current demand. Yields fluctuate with market conditions and aren't guaranteed, but the underlying mechanism, lending to over-collateralized borrowers on audited protocols, is real and operational at scale.

How much money do you need to start earning crypto yield online?

There's no technical minimum. Compound and Morpho accept any deposit size. Practically speaking, a few hundred dollars is where the yield becomes meaningfully visible relative to gas costs (though Pistachio covers those fees entirely for its users). At $1,000 deposited and 6% APY, you'd earn roughly $60 in a year, paid continuously without any additional input.

Is DeFi yield income taxable?

In the US and most jurisdictions, yes. Yield earned on crypto lending or staking is generally treated as ordinary income at the time it's received, similar to bank interest. The dollar value at the time of receipt is what's reportable. Pistachio integrates with Awaken.Tax for one-tap portfolio export, which simplifies the record-keeping significantly.

What's the difference between ETH staking and stablecoin lending?

Both earn yield, but they carry different risk profiles. ETH staking earns 3-4% APY but your principal is in ETH, which moves with crypto markets. If ETH drops 20%, your dollar value drops even while yield accrues. Stablecoin lending keeps your principal in USDC (pegged to $1) and earns 4-10% APY, so you're earning yield without taking on crypto price exposure. Stablecoin lending carries stablecoin peg risk and protocol smart contract risk, but no ETH price risk.

How is earning money online with crypto different from trading?

Trading involves actively buying and selling assets to profit from price movements. It requires time, analysis, and skill, and most retail traders lose money relative to simply holding. Crypto yield is passive: you deposit assets into a lending protocol or staking mechanism and earn interest, with no active management required. The return profile is also different: yield is steady and predictable (within normal rate ranges), while trading profits are highly variable.

Cross-chain crypto swaps: how Li.Fi powers Pistachio's one-tap zaps (2026)

Etherfuse stablebonds: earn government bond yields on-chain (2026)

How to earn money online in 2026 (crypto yield vs. the rest)

Linea crypto explained: what it is and how it works (2026)

Ethereum wallet guide 2026 (ethernet wallet explained)

DeFi Staking with Stader Labs: How ETHx Works in 2026

High-liquidity crypto exchanges: PancakeSwap guide 2026

What is Raydium? How Solana's AMM Works in 2026

Passive Income Ideas for 2026: 10 Ways That Actually Work

Hong Kong crypto news 2026: licenses, stablecoins, and regulation

©2026 Copyright, PistachioFi Inc.

©2026 Copyright, PistachioFi Inc.

©2026 Copyright, PistachioFi Inc.