Best crypto neobank 2026: earn, spend, and grow your money

Best crypto neobank 2026: earn, spend, and grow your money

Best crypto neobank 2026: earn, spend, and grow your money

Best crypto neobank 2026: earn, spend, and grow your money

Most crypto neobank lists rank platforms by how many coins you can trade or what color their card is. That misses the point. The best crypto neobank in 2026 should do more than help you spend. It should help you earn while your money sits there.

The crypto neobank space has split into three camps: traditional banks bolting on crypto features, crypto-native platforms adding banking layers, and yield-first platforms that treat earning as the default. We looked at each category and compared them on what actually matters: yield, fees, self-custody, and whether your idle stablecoins are working for you or just sitting in a wallet.

Pistachio.fi is a crypto yield platform that gives you access to curated investment vaults with expert risk grades, completely gasless transactions, and built-in tax tracking through Awaken.Tax integration. It fits the yield-first category, and we will explain why that matters throughout this guide.

In this article

Which crypto neobanks offer real yield on idle assets (not just cashback gimmicks)

How the best crypto neobank in 2026 compares on fees, custody, and earning potential

Why yield-first platforms outperform traditional crypto friendly banks for long-term holders

The specific tradeoffs between spending-focused and earning-focused neobanks

Where Pistachio.fi fits and when it makes more sense than a traditional crypto neobank

What is a crypto neobank and why does yield matter?

A crypto neobank is a digital-only financial platform that combines traditional banking functions (spending, saving, transfers) with cryptocurrency support. Some let you buy and hold crypto. Others let you spend it with a card. A few actually let you earn meaningful returns on your holdings.

Here is the problem with most crypto neobanks: they are optimized for transactions, not growth. You deposit stablecoins, you get a shiny card, you spend them. Your balance goes down over time. That is a spending tool, not a financial platform.

Yield changes the equation. When your stablecoins earn 5-13% annually through lending protocols or real-world asset vaults, your money grows between purchases. That is the difference between a crypto neobank that costs you money and one that makes you money.

How we evaluated the top crypto neobanks

We scored each platform across five categories:

Yield on deposits (stablecoins, BTC, ETH)

Fee structure (trading fees, card fees, hidden costs)

Custody model (custodial vs. self-custody)

Card and spending features (cashback, supported currencies)

Risk transparency (do they explain how yield is generated?)

Platforms that scored high on yield and transparency ranked highest. A 2% cashback card means nothing if you are losing 8% in opportunity cost by not earning on your idle balance.

Crypto neobank comparison: the full breakdown

Here is how the major players stack up across the features that matter most.

Platform | Yield on stablecoins | Cashback | Custody | Card type | Monthly fee | Best for |

|---|---|---|---|---|---|---|

Pistachio.fi | Up to 13% (vaults) | N/A | Self-custody | No card (yield-first) | Free | Earning on idle crypto |

ether.fi | Variable (liquid vaults) | 2-3% | Self-custody | Visa | Free (tier-based perks) | DeFi-native spenders |

Revolut | Up to 5.5% (fiat only) | Tier-dependent | Custodial | Visa/Mastercard | Free-$18/mo | Mainstream crypto + banking |

Wirex | Up to 20% (with WXT lock) | 0.5-8% (in WXT) | Custodial | Visa/Mastercard | Free-$30/mo | Cashback maximizers |

Nexo | Up to 14% (USDC) | Up to 2% | Custodial | Mastercard | Free | Earning + credit line |

Xapo Bank | 0.5% BTC / 3.6% USD | None | Custodial | Mastercard | Membership-based | Bitcoin holders |

Gnosis Pay | None (spending only) | 1-4% (in GNO) | Self-custody | Visa | ~$30 issuance | On-chain purists |

Bleap | None (spending only) | 2% (in USDC) | Self-custody (MPC) | Visa | Free | USDC spenders |

Rates as of February 2026. Yields are variable and depend on market conditions, platform tiers, and token lockup requirements. Always verify current rates directly with each platform.

Which crypto neobanks actually pay you to hold?

Only a handful of platforms in this comparison generate meaningful yield on your deposits. Let's break down what "yield" actually means at each one, because the headline numbers can be misleading.

Pistachio.fi routes your deposits into curated DeFi lending protocols and real-world asset (RWA) vaults. Yields range from roughly 5% on conservative stablecoin lending up to 13% on higher-tier vaults. Every vault carries an expert risk grade so you can see exactly what you are getting into. There are no gas fees, no token lockups, and no native token you need to buy first. If you want to understand more about how these returns work, our guide on passive income with crypto in 2026 breaks down the mechanics.

Nexo offers solid rates, up to 14% on USDC for Platinum-tier members using fixed terms. The catch: reaching Platinum requires holding a significant portion of your portfolio in NEXO tokens. The base rate without any NEXO holdings is considerably lower. The card is also limited to EEA and UK residents.

Wirex advertises up to 20% on X-Accounts, but that top rate requires their Elite tier ($30/month) plus locking WXT tokens for 180 days. The standard tier without any WXT lockup offers up to 9%. Their cashback of up to 8% is also paid in WXT, so your real return depends on that token's price stability.

Revolut pays up to 5.5% APY on USD savings for Metal plan members, but only on fiat, not crypto. Their crypto offering is trading-focused with fees from 0.49% to 1.49% per trade depending on your plan. No stablecoin yield.

Xapo Bank takes the most conservative approach with 0.5% APR on up to 5 BTC and 3.6% on USD. They never lend your Bitcoin, which is a strong selling point for security-minded holders, but the yields reflect that caution. Their BTC Credit Fund targets 5% APY but requires a $100,000 minimum.

What about spending-focused platforms?

If you primarily want to spend crypto with a card, ether.fi, Gnosis Pay, and Bleap each take a different approach.

ether.fi Cash works as a crypto-native Visa card where you pledge staked ETH (eETH) or stablecoins as collateral and borrow against them. You keep earning staking yield on your collateral while spending. The 2-3% cashback is solid, and the self-custodial model means your keys stay yours. The downside: it is built around the Ethereum ecosystem, so if you are not already an ETH holder, the onboarding has friction.

Gnosis Pay runs on a Safe smart wallet on Gnosis Chain. It is the most "crypto-native" card out there. But there is a 1.5% stabilization fee on every transaction, and cashback is paid in GNO tokens. Good for on-chain believers. Less practical for everyone else.

Bleap takes the simplest approach. Spend USDC, get 2% cashback in USDC. No volatile token rewards, no complicated tier systems. The tradeoff: zero yield on your balance. Your USDC just sits there until you spend it.

Why yield-first platforms are winning the crypto neobank race

Here is the math that most crypto neobank comparison articles ignore.

Say you hold $10,000 in stablecoins. On a spending-only platform, you get a card and maybe 2% cashback. If you spend $2,000 per month, that is $40 back monthly, or $480 per year.

On a yield-first platform like Pistachio.fi earning 8% on your idle balance, you make $800 per year in yield on that same $10,000, without spending a dollar. If you want a card, you can use a separate spending platform for the portion you actually need to spend.

The point is not that spending cards are bad. The point is that yield should come first. Earn on the bulk of your holdings, then allocate a smaller portion to a spending card if you need one. For a deeper comparison of yield options versus traditional savings, check our breakdown of the best high-yield savings accounts in 2026.

How does Pistachio.fi compare as a crypto yield platform?

Pistachio.fi is not a neobank in the traditional sense. There is no card, no fiat on-ramp, no checking account. It is a specialized yield platform, and that focus is what makes it worth including in this comparison.

Here is what sets it apart:

Curated investment vaults. Instead of dumping you into a single yield product, Pistachio gives you a menu of vaults with different risk and return profiles. Stablecoin lending, RWA-backed vaults, and blue-chip crypto yield options are all available. Each vault is audited multiple times over.

Expert risk grades. Every vault shows a clear risk rating. You do not need to research protocols yourself or guess whether a 15% APY is too good to be true. The platform does that analysis for you.

Completely gasless. No gas fees on deposits, withdrawals, or vault switches. This sounds small, but gas costs on Ethereum mainnet can eat into yield fast, especially on smaller balances.

Awaken.Tax integration. Built-in tax tracking so you are not scrambling at year-end to figure out your DeFi income. This alone saves hours for anyone earning across multiple vaults.

Self-custody. You hold your own keys. Your funds are not sitting on an exchange balance sheet. After FTX and Celsius, that distinction is worth repeating.

The platform currently supports deposits on Base, Arbitrum, Optimism, Scroll, Mantle, BNB, and Polygon, with more chains coming. If you care about how your funds are protected, Pistachio publishes detailed security documentation covering their wallet infrastructure and audit history.

What should you look for in a crypto friendly bank?

Choosing the right platform depends on what you actually need. Here is a practical framework:

If you mostly hold and rarely spend crypto, a yield-first platform like Pistachio.fi or Nexo makes the most sense. Your priority is earning returns, not card perks.

If you spend crypto weekly, ether.fi Cash or Bleap give you self-custodial spending with decent cashback. Pair one with a yield platform for idle funds.

If you want one app for everything, Revolut is the most polished all-in-one option, but you sacrifice yield on crypto holdings and pay higher trading fees on the free plan.

If you are a Bitcoin maximalist, Xapo Bank is purpose-built for you, though the yields are modest. Their never-lend-your-BTC approach is the selling point, not the returns.

If you are chasing the highest advertised APY, read the fine print. Wirex's 20% requires a paid tier and token lockups. Nexo's 14% requires Platinum status and NEXO token holdings. The "up to" number is rarely the number you will actually get.

FAQ

What is the safest crypto neobank in 2026?

Safety depends on the custody model. Self-custodial platforms like Pistachio.fi, ether.fi, and Gnosis Pay do not hold your funds, which eliminates exchange insolvency risk. Among custodial options, Xapo Bank (regulated in Gibraltar by the GFSC) and Revolut (UK banking license) have the strongest regulatory backing. For yield platforms specifically, look for audited smart contracts, transparent risk disclosures, and no history of exploits.

Can you earn interest on stablecoins with a crypto neobank?

Yes, but the rates and mechanisms vary widely. Nexo offers up to 14% APY on USDC for top-tier members. Wirex pays up to 20% on X-Accounts with token lockups. Pistachio.fi offers up to 13% through curated DeFi vaults without requiring a native token. Spending-focused platforms like Bleap and Gnosis Pay do not offer any yield on idle balances. Always check whether the advertised rate requires a paid subscription, token holdings, or lockup period.

Do crypto neobanks charge hidden fees?

Many do. Revolut charges 1.49% per crypto trade on its free plan. Gnosis Pay applies a 1.5% stabilization fee on card transactions. Wirex's headline cashback rates require paid tiers ($10-$30/month) and WXT token lockups. Even "free" platforms generate revenue somehow, usually through spreads on conversions or by lending your deposits. The most transparent platforms, including Pistachio.fi, clearly show how yield is generated and what fees (if any) apply before you deposit.

Is a crypto neobank better than a regular bank for savings?

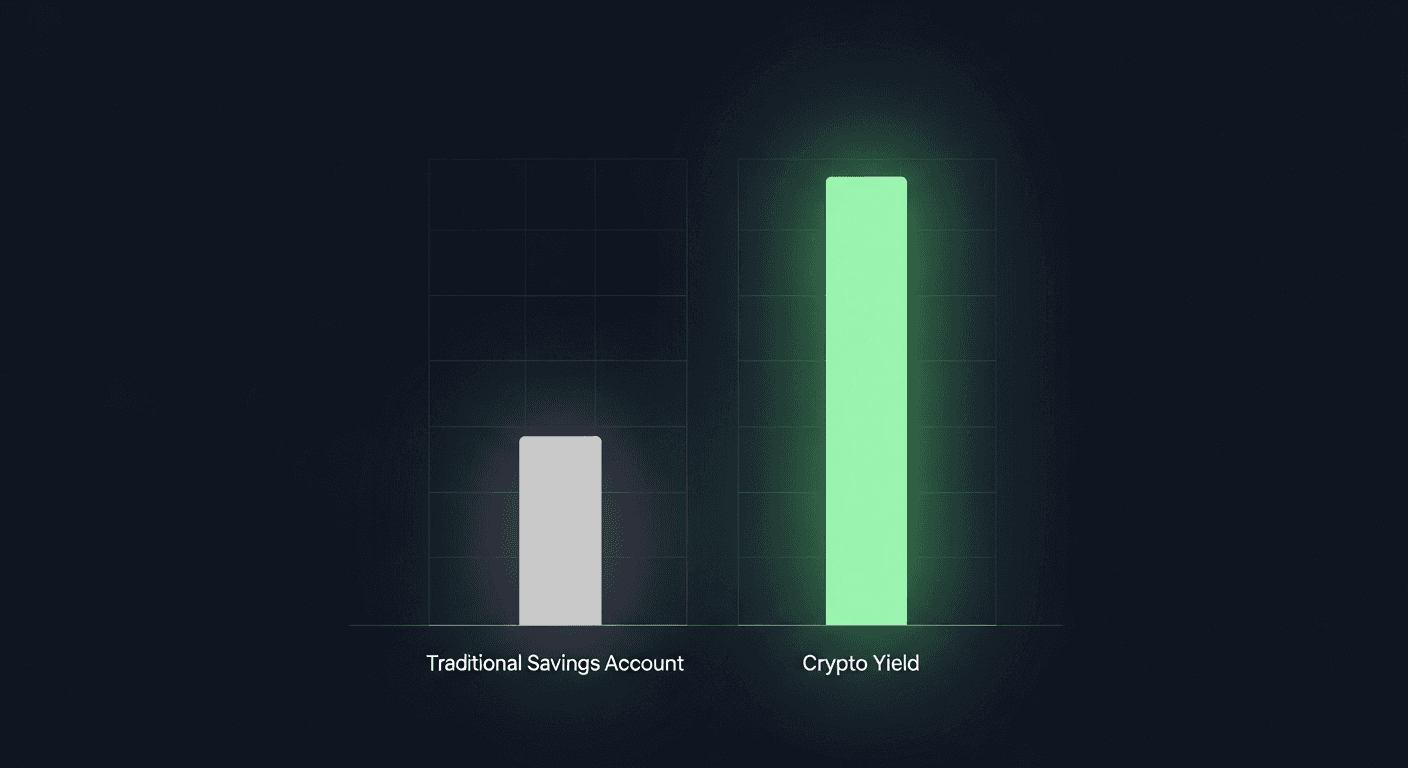

For yield on stablecoins, crypto platforms consistently outperform traditional savings accounts. The average US savings account pays around 0.5% APY. Even Revolut's high-yield account at 5.5% (Metal plan) beats most banks. DeFi-based yield platforms like Pistachio.fi can offer 5-13% depending on the vault. The tradeoff is that crypto yields carry smart contract risk and are not FDIC insured. If you are comfortable with those risks and want to understand the comparison in detail, read our guide to high-yield savings options in 2026.

How do crypto neobank cashback rewards work?

Cashback on crypto cards works similarly to traditional cards but with a twist: rewards are often paid in the platform's native token rather than cash or stablecoins. Wirex pays in WXT, Gnosis Pay in GNO, and ether.fi in ETHFI tokens. This means your actual cashback value fluctuates with token prices. Bleap is a notable exception, paying 2% back in USDC. When comparing cashback rates, always check what currency the reward is paid in and whether you need a paid subscription to unlock the advertised rate.

Last updated: February 2026. Rates, features, and availability change frequently. Verify all figures directly with each platform before making financial decisions.

This article is for informational purposes only and does not constitute financial advice. Crypto investments carry risk, including potential loss of principal.

Most crypto neobank lists rank platforms by how many coins you can trade or what color their card is. That misses the point. The best crypto neobank in 2026 should do more than help you spend. It should help you earn while your money sits there.

The crypto neobank space has split into three camps: traditional banks bolting on crypto features, crypto-native platforms adding banking layers, and yield-first platforms that treat earning as the default. We looked at each category and compared them on what actually matters: yield, fees, self-custody, and whether your idle stablecoins are working for you or just sitting in a wallet.

Pistachio.fi is a crypto yield platform that gives you access to curated investment vaults with expert risk grades, completely gasless transactions, and built-in tax tracking through Awaken.Tax integration. It fits the yield-first category, and we will explain why that matters throughout this guide.

In this article

Which crypto neobanks offer real yield on idle assets (not just cashback gimmicks)

How the best crypto neobank in 2026 compares on fees, custody, and earning potential

Why yield-first platforms outperform traditional crypto friendly banks for long-term holders

The specific tradeoffs between spending-focused and earning-focused neobanks

Where Pistachio.fi fits and when it makes more sense than a traditional crypto neobank

What is a crypto neobank and why does yield matter?

A crypto neobank is a digital-only financial platform that combines traditional banking functions (spending, saving, transfers) with cryptocurrency support. Some let you buy and hold crypto. Others let you spend it with a card. A few actually let you earn meaningful returns on your holdings.

Here is the problem with most crypto neobanks: they are optimized for transactions, not growth. You deposit stablecoins, you get a shiny card, you spend them. Your balance goes down over time. That is a spending tool, not a financial platform.

Yield changes the equation. When your stablecoins earn 5-13% annually through lending protocols or real-world asset vaults, your money grows between purchases. That is the difference between a crypto neobank that costs you money and one that makes you money.

How we evaluated the top crypto neobanks

We scored each platform across five categories:

Yield on deposits (stablecoins, BTC, ETH)

Fee structure (trading fees, card fees, hidden costs)

Custody model (custodial vs. self-custody)

Card and spending features (cashback, supported currencies)

Risk transparency (do they explain how yield is generated?)

Platforms that scored high on yield and transparency ranked highest. A 2% cashback card means nothing if you are losing 8% in opportunity cost by not earning on your idle balance.

Crypto neobank comparison: the full breakdown

Here is how the major players stack up across the features that matter most.

Platform | Yield on stablecoins | Cashback | Custody | Card type | Monthly fee | Best for |

|---|---|---|---|---|---|---|

Pistachio.fi | Up to 13% (vaults) | N/A | Self-custody | No card (yield-first) | Free | Earning on idle crypto |

ether.fi | Variable (liquid vaults) | 2-3% | Self-custody | Visa | Free (tier-based perks) | DeFi-native spenders |

Revolut | Up to 5.5% (fiat only) | Tier-dependent | Custodial | Visa/Mastercard | Free-$18/mo | Mainstream crypto + banking |

Wirex | Up to 20% (with WXT lock) | 0.5-8% (in WXT) | Custodial | Visa/Mastercard | Free-$30/mo | Cashback maximizers |

Nexo | Up to 14% (USDC) | Up to 2% | Custodial | Mastercard | Free | Earning + credit line |

Xapo Bank | 0.5% BTC / 3.6% USD | None | Custodial | Mastercard | Membership-based | Bitcoin holders |

Gnosis Pay | None (spending only) | 1-4% (in GNO) | Self-custody | Visa | ~$30 issuance | On-chain purists |

Bleap | None (spending only) | 2% (in USDC) | Self-custody (MPC) | Visa | Free | USDC spenders |

Rates as of February 2026. Yields are variable and depend on market conditions, platform tiers, and token lockup requirements. Always verify current rates directly with each platform.

Which crypto neobanks actually pay you to hold?

Only a handful of platforms in this comparison generate meaningful yield on your deposits. Let's break down what "yield" actually means at each one, because the headline numbers can be misleading.

Pistachio.fi routes your deposits into curated DeFi lending protocols and real-world asset (RWA) vaults. Yields range from roughly 5% on conservative stablecoin lending up to 13% on higher-tier vaults. Every vault carries an expert risk grade so you can see exactly what you are getting into. There are no gas fees, no token lockups, and no native token you need to buy first. If you want to understand more about how these returns work, our guide on passive income with crypto in 2026 breaks down the mechanics.

Nexo offers solid rates, up to 14% on USDC for Platinum-tier members using fixed terms. The catch: reaching Platinum requires holding a significant portion of your portfolio in NEXO tokens. The base rate without any NEXO holdings is considerably lower. The card is also limited to EEA and UK residents.

Wirex advertises up to 20% on X-Accounts, but that top rate requires their Elite tier ($30/month) plus locking WXT tokens for 180 days. The standard tier without any WXT lockup offers up to 9%. Their cashback of up to 8% is also paid in WXT, so your real return depends on that token's price stability.

Revolut pays up to 5.5% APY on USD savings for Metal plan members, but only on fiat, not crypto. Their crypto offering is trading-focused with fees from 0.49% to 1.49% per trade depending on your plan. No stablecoin yield.

Xapo Bank takes the most conservative approach with 0.5% APR on up to 5 BTC and 3.6% on USD. They never lend your Bitcoin, which is a strong selling point for security-minded holders, but the yields reflect that caution. Their BTC Credit Fund targets 5% APY but requires a $100,000 minimum.

What about spending-focused platforms?

If you primarily want to spend crypto with a card, ether.fi, Gnosis Pay, and Bleap each take a different approach.

ether.fi Cash works as a crypto-native Visa card where you pledge staked ETH (eETH) or stablecoins as collateral and borrow against them. You keep earning staking yield on your collateral while spending. The 2-3% cashback is solid, and the self-custodial model means your keys stay yours. The downside: it is built around the Ethereum ecosystem, so if you are not already an ETH holder, the onboarding has friction.

Gnosis Pay runs on a Safe smart wallet on Gnosis Chain. It is the most "crypto-native" card out there. But there is a 1.5% stabilization fee on every transaction, and cashback is paid in GNO tokens. Good for on-chain believers. Less practical for everyone else.

Bleap takes the simplest approach. Spend USDC, get 2% cashback in USDC. No volatile token rewards, no complicated tier systems. The tradeoff: zero yield on your balance. Your USDC just sits there until you spend it.

Why yield-first platforms are winning the crypto neobank race

Here is the math that most crypto neobank comparison articles ignore.

Say you hold $10,000 in stablecoins. On a spending-only platform, you get a card and maybe 2% cashback. If you spend $2,000 per month, that is $40 back monthly, or $480 per year.

On a yield-first platform like Pistachio.fi earning 8% on your idle balance, you make $800 per year in yield on that same $10,000, without spending a dollar. If you want a card, you can use a separate spending platform for the portion you actually need to spend.

The point is not that spending cards are bad. The point is that yield should come first. Earn on the bulk of your holdings, then allocate a smaller portion to a spending card if you need one. For a deeper comparison of yield options versus traditional savings, check our breakdown of the best high-yield savings accounts in 2026.

How does Pistachio.fi compare as a crypto yield platform?

Pistachio.fi is not a neobank in the traditional sense. There is no card, no fiat on-ramp, no checking account. It is a specialized yield platform, and that focus is what makes it worth including in this comparison.

Here is what sets it apart:

Curated investment vaults. Instead of dumping you into a single yield product, Pistachio gives you a menu of vaults with different risk and return profiles. Stablecoin lending, RWA-backed vaults, and blue-chip crypto yield options are all available. Each vault is audited multiple times over.

Expert risk grades. Every vault shows a clear risk rating. You do not need to research protocols yourself or guess whether a 15% APY is too good to be true. The platform does that analysis for you.

Completely gasless. No gas fees on deposits, withdrawals, or vault switches. This sounds small, but gas costs on Ethereum mainnet can eat into yield fast, especially on smaller balances.

Awaken.Tax integration. Built-in tax tracking so you are not scrambling at year-end to figure out your DeFi income. This alone saves hours for anyone earning across multiple vaults.

Self-custody. You hold your own keys. Your funds are not sitting on an exchange balance sheet. After FTX and Celsius, that distinction is worth repeating.

The platform currently supports deposits on Base, Arbitrum, Optimism, Scroll, Mantle, BNB, and Polygon, with more chains coming. If you care about how your funds are protected, Pistachio publishes detailed security documentation covering their wallet infrastructure and audit history.

What should you look for in a crypto friendly bank?

Choosing the right platform depends on what you actually need. Here is a practical framework:

If you mostly hold and rarely spend crypto, a yield-first platform like Pistachio.fi or Nexo makes the most sense. Your priority is earning returns, not card perks.

If you spend crypto weekly, ether.fi Cash or Bleap give you self-custodial spending with decent cashback. Pair one with a yield platform for idle funds.

If you want one app for everything, Revolut is the most polished all-in-one option, but you sacrifice yield on crypto holdings and pay higher trading fees on the free plan.

If you are a Bitcoin maximalist, Xapo Bank is purpose-built for you, though the yields are modest. Their never-lend-your-BTC approach is the selling point, not the returns.

If you are chasing the highest advertised APY, read the fine print. Wirex's 20% requires a paid tier and token lockups. Nexo's 14% requires Platinum status and NEXO token holdings. The "up to" number is rarely the number you will actually get.

FAQ

What is the safest crypto neobank in 2026?

Safety depends on the custody model. Self-custodial platforms like Pistachio.fi, ether.fi, and Gnosis Pay do not hold your funds, which eliminates exchange insolvency risk. Among custodial options, Xapo Bank (regulated in Gibraltar by the GFSC) and Revolut (UK banking license) have the strongest regulatory backing. For yield platforms specifically, look for audited smart contracts, transparent risk disclosures, and no history of exploits.

Can you earn interest on stablecoins with a crypto neobank?

Yes, but the rates and mechanisms vary widely. Nexo offers up to 14% APY on USDC for top-tier members. Wirex pays up to 20% on X-Accounts with token lockups. Pistachio.fi offers up to 13% through curated DeFi vaults without requiring a native token. Spending-focused platforms like Bleap and Gnosis Pay do not offer any yield on idle balances. Always check whether the advertised rate requires a paid subscription, token holdings, or lockup period.

Do crypto neobanks charge hidden fees?

Many do. Revolut charges 1.49% per crypto trade on its free plan. Gnosis Pay applies a 1.5% stabilization fee on card transactions. Wirex's headline cashback rates require paid tiers ($10-$30/month) and WXT token lockups. Even "free" platforms generate revenue somehow, usually through spreads on conversions or by lending your deposits. The most transparent platforms, including Pistachio.fi, clearly show how yield is generated and what fees (if any) apply before you deposit.

Is a crypto neobank better than a regular bank for savings?

For yield on stablecoins, crypto platforms consistently outperform traditional savings accounts. The average US savings account pays around 0.5% APY. Even Revolut's high-yield account at 5.5% (Metal plan) beats most banks. DeFi-based yield platforms like Pistachio.fi can offer 5-13% depending on the vault. The tradeoff is that crypto yields carry smart contract risk and are not FDIC insured. If you are comfortable with those risks and want to understand the comparison in detail, read our guide to high-yield savings options in 2026.

How do crypto neobank cashback rewards work?

Cashback on crypto cards works similarly to traditional cards but with a twist: rewards are often paid in the platform's native token rather than cash or stablecoins. Wirex pays in WXT, Gnosis Pay in GNO, and ether.fi in ETHFI tokens. This means your actual cashback value fluctuates with token prices. Bleap is a notable exception, paying 2% back in USDC. When comparing cashback rates, always check what currency the reward is paid in and whether you need a paid subscription to unlock the advertised rate.

Last updated: February 2026. Rates, features, and availability change frequently. Verify all figures directly with each platform before making financial decisions.

This article is for informational purposes only and does not constitute financial advice. Crypto investments carry risk, including potential loss of principal.

Cross-chain crypto swaps: how Li.Fi powers Pistachio's one-tap zaps (2026)

Etherfuse stablebonds: earn government bond yields on-chain (2026)

How to earn money online in 2026 (crypto yield vs. the rest)

Linea crypto explained: what it is and how it works (2026)

Ethereum wallet guide 2026 (ethernet wallet explained)

DeFi Staking with Stader Labs: How ETHx Works in 2026

High-liquidity crypto exchanges: PancakeSwap guide 2026

What is Raydium? How Solana's AMM Works in 2026

Passive Income Ideas for 2026: 10 Ways That Actually Work

Hong Kong crypto news 2026: licenses, stablecoins, and regulation

©2026 Copyright, PistachioFi Inc.

©2026 Copyright, PistachioFi Inc.

©2026 Copyright, PistachioFi Inc.